Can You Trust an AI Financial Advisor? How Accurate It Really Is (and How to Use It Safely)

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

Yes, you can generally trust an AI financial advisor as a learning tool and a useful first step — but not as a final word. Its answers can sound completely confident while still being wrong, so treat every number and rule it gives you as a draft to verify against a primary source, and bring complex, high-stakes decisions to a licensed professional.

Millions of people now ask AI chatbots about money, from budgeting basics to retirement math. This guide walks through what independent tests actually found, exactly where an AI-powered financial advisor tends to go wrong, and how to check its answers before you act on them.

How Accurate Is an AI Financial Advisor, Really?

Independent grading paints a mixed picture: solid on explaining concepts, shakier the moment specifics enter the conversation.

The honest answer: strong for concepts, shaky on specifics

An AI financial advice tool is genuinely good at explaining concepts — what a Roth IRA is, how compound interest works, or how an index fund differs from an actively managed one — and it can help structure your thinking around a decision. Where reliability drops is specifics: exact figures, current-year rules, and calculations tailored to your actual situation. A useful way to hold both truths at once: strong for education, shaky for precise, personal answers you’d act on directly.

What independent tests and studies show

Money magazine graded ChatGPT o3 against Google Gemini 2.5 Pro across 25 personal-finance questions, with five evaluators producing 250 total scores. Both models landed in the B range — reasonably solid overall, but with real mistakes mixed in. Separately, a study in the Journal of Financial Planning that queried seven generative AI platforms (ChatGPT, Claude, Copilot, DeepSeek, Gemini, Meta AI, and Perplexity) in August 2025 found «substantial variation» in the advice given on emergency savings targets and portfolio allocation — meaning the same question produced noticeably different answers depending on which tool you asked. Safe-withdrawal-rate advice was the one area where the platforms mostly agreed, with most tools pointing to something close to the traditional 4% rule. Adoption is already high: Pew Research found 34% of US adults, and 58% of adults under 30, have used ChatGPT. The takeaway is consistent across both studies: an AI chatbot for money can be useful, but it isn’t stable, and it isn’t a single source of truth.

| Study | What it tested | Key finding |

|---|---|---|

| Money (ChatGPT o3 vs. Gemini 2.5 Pro) | 25 questions, 5 evaluators, 250 scores | Both models graded in the B range, with notable errors |

| Journal of Financial Planning | 7 GenAI platforms on savings, withdrawal rate, allocation | «Substantial variation» on savings and allocation; withdrawal-rate advice was comparatively consistent |

Why AI Sounds Confident but Can Still Be Wrong

The tone of an answer and its accuracy are two different things — and that gap is exactly where AI financial advice can mislead you.

A large language model predicts the next likely word, not the truth. That single fact explains most of what goes wrong. The model isn’t checking a fact database before it answers; it’s generating the most statistically plausible continuation of your question, which is why it can state a nonexistent relief program, the wrong contribution limit, or an invented interest rate — always in the same confident tone. Andrew Lo, a professor at MIT’s Laboratory for Financial Engineering, put it directly:

No matter what you ask it, it’ll always come back with an answer that sounds authoritative, even if it’s not.

Andrew Lo, MIT Laboratory for Financial Engineering

Hallucination is the technical name for this. It refers to a large language model producing a plausible-sounding but false or fabricated answer — not a lie in the human sense, just a confident guess dressed up as a fact. NIST, the US National Institute of Standards and Technology, tracks hallucination as a known, documented risk category for generative AI systems, not a rare edge case.

Prompt sensitivity compounds the problem. Small changes in how you phrase a question can change the recommendation you get back. That means a single AI answer isn’t an objective verdict — it’s a function of exactly how you asked. The practical fix is to rephrase your question a few different ways and compare what comes back rather than trusting the first answer.

The Outdated-Information Problem (Knowledge Cutoff)

Every large language model has a training cutoff date, and money rules keep changing after that date passes.

Money rules change every year — models may not know

Many of the numbers that matter most in personal finance are updated annually: federal tax brackets, the standard deduction, and contribution limits for IRAs and 401(k)s. A model trained with a knowledge cutoff can present last year’s figure — or an even older one — as if it were current. This isn’t hypothetical: ChatGPT incorrectly described the Fresh Start program for federal student loans as «still available» months after it had actually ended in fall 2024, and Gemini cited outdated 2024 auto-loan figures in a response given in June 2025. Earlier ChatGPT versions were even more limited by comparison — the original GPT-4 model’s investment answers were bound by a September 2021 knowledge cutoff.

Always assume numbers may be stale

The practical rule: treat any specific number an AI financial advisor gives you — a limit, a rate, a threshold, a deadline — as a draft, not a fact, and confirm it against a primary source before you rely on it, especially anything touching taxes or retirement contributions.

AI Has No Fiduciary Duty — Why That Matters

A licensed advisor and an AI chatbot may sound equally confident, but only one of them is legally required to act in your interest.

What «fiduciary» means and why AI isn’t one

A fiduciary is legally obligated to put your interests ahead of their own. A licensed human financial advisor acting as a fiduciary carries that legal duty and the accountability that comes with it. An AI-powered financial advisor carries neither — it has no legal obligation to act in your favor and no accountability if its answer costs you money.

AI doesn’t know your full picture

An AI tool doesn’t see your complete financial picture — your income, debts, tax situation, risk tolerance, or family goals — unless you type all of it in yourself, and typing in sensitive financial details carries its own privacy risk. Without that full context, what looks like personal advice is really a general answer dressed up to sound specific to you.

What You Must Always Verify (Against Primary Sources)

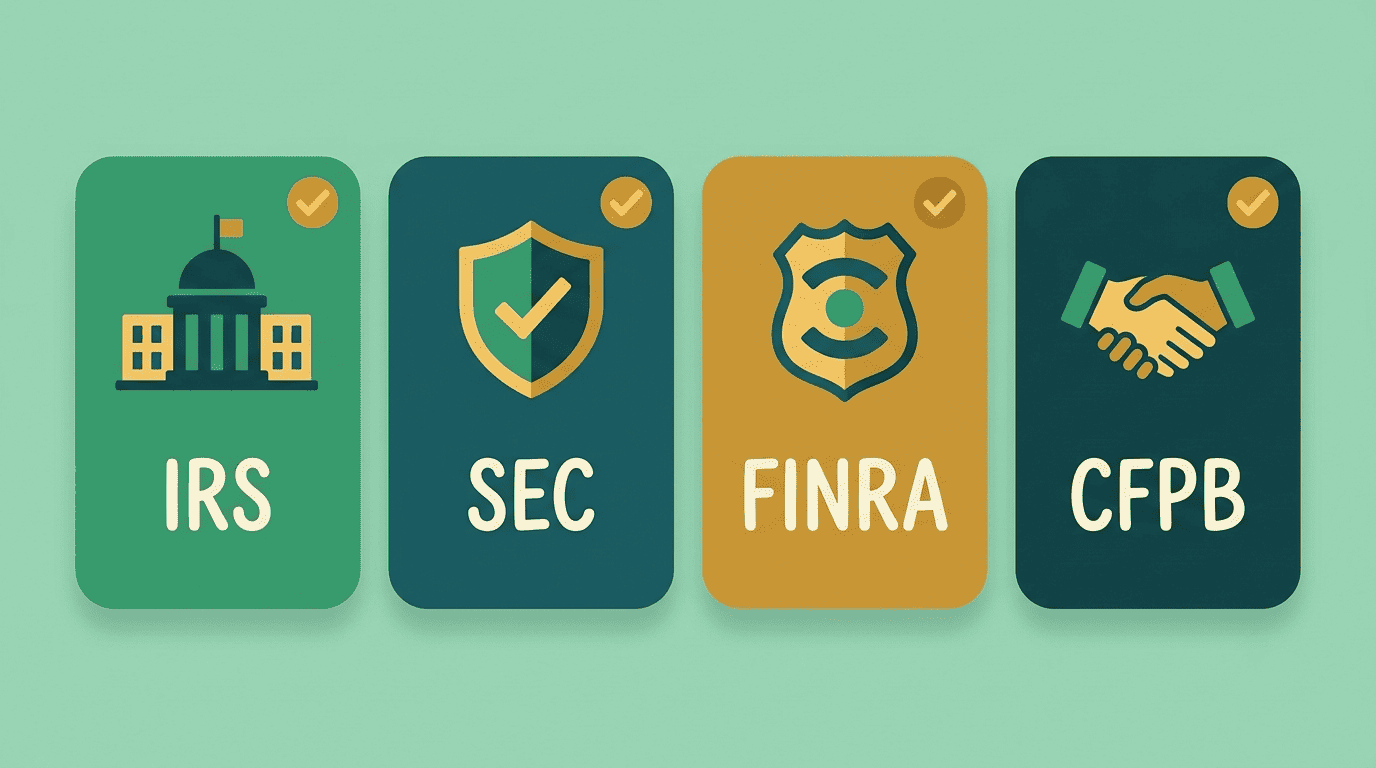

Certain categories of information should never be taken from an AI chatbot at face value — they need to be checked against the agency that actually sets the rule.

Tax brackets, deductions, contribution limits → IRS

Any tax figure or retirement contribution limit should be checked directly on IRS.gov, which publishes the official, current-year numbers.

Advisors, brokers, regulation → SEC / FINRA

Before acting on any investment recommendation, or before trusting a specific advisor or broker, check Investor.gov (run by the SEC) and FINRA BrokerCheck. An AI tool can invent or misstate a fact; a regulator’s public record doesn’t.

Consumer protection & complaints → CFPB

Questions involving credit, debt, loans, or consumer rights belong in front of the Consumer Financial Protection Bureau (CFPB), which handles exactly this category of complaint and guidance.

Here’s a simple way to keep the mapping straight:

| What the AI told you | Where to verify it |

|---|---|

| A tax bracket, deduction, or IRA/401(k) limit | IRS.gov |

| Whether an advisor or broker is legitimate | Investor.gov (SEC) / FINRA BrokerCheck |

| A consumer-credit or debt question | CFPB |

| An interest-rate or economic figure | Federal Reserve |

Prompt Tips: Getting Safer Answers from AI

How you ask shapes what you get back — a few habits meaningfully lower the odds of an unverified answer slipping through.

Ask for sources, dates, and step-by-step math

Before you act on any specific figure, it helps to ask the AI directly for:

- The source it drew the figure from

- The year or date the data is current as of

- A step-by-step calculation, so you can catch an arithmetic error yourself

- Any assumptions it made along the way

If it can’t point to a source, treat that as a signal to double-check the answer elsewhere.

Avoid leading questions; ask it to flag uncertainty

Skip leading questions like «confirm that X is a good idea» — they push the model toward agreement rather than accuracy. Instead, ask neutrally: «Where could you be wrong here?» or «What should I confirm with a professional?» Rephrasing the same question a few different ways and comparing the answers is one of the simplest ways to catch prompt-sensitivity errors.

Protect Your Data: Privacy of What You Type

What you type into a chat window doesn’t necessarily disappear after the conversation ends.

AI chat sessions can be retained for an extended period and may be accessible to third parties or used to help train future models. Avoid typing full account numbers, Social Security numbers, complete financial statements, or an exact date of birth into a general-purpose AI chatbot. Use rounded, generalized figures («around $X») instead of exact identifiers whenever you’re asking a money question.

When to Use AI vs. When to See a Licensed Advisor

The line isn’t «AI or a human» — it’s knowing which category your question falls into.

Great for learning and getting oriented

An AI financial advisor tool is genuinely useful for:

- Understanding financial terms and concepts

- Sketching a rough first-draft budget

- Preparing a list of questions before a meeting with an advisor

- Comparing concepts side by side (e.g., Roth vs. traditional IRA)

Use it as a tutor that helps you get oriented, not as the body that hands down the final decision.

See a professional for high-stakes, complex, or personal decisions

Bring a licensed advisor into decisions involving:

- Social Security claiming timing

- Tax planning and required minimum distributions (RMDs)

- Large investment moves

- Dividing assets in a divorce

- Estate planning

- Significant debt

The stakes are high in each of these categories, and a confidently wrong AI answer here can be expensive to unwind.

A Safe-Use Checklist for AI Financial Answers

Pulling every rule above into one sequence makes it easy to run through before you act on anything an AI tool tells you.

The 7-point checklist

- Treat every AI answer as a draft, not a final decision.

- Verify every specific number against a primary source — IRS, SEC/Investor.gov, or CFPB.

- Ask the AI for its source, the date of the data, and a step-by-step calculation.

- Never paste account numbers, SSNs, or other sensitive identifiers into a chat.

- Avoid leading questions; ask the AI to flag where it could be wrong.

- Bring large, complex, or high-stakes decisions to a licensed advisor.

- Remember an AI financial advisor carries no fiduciary duty toward you.