Are AI Financial Advisors Regulated? What the SEC, FINRA, and Fiduciary Duty Actually Cover

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

The short answer is nuanced: a licensed AI financial advisor that is registered with the SEC is regulated like any other adviser, but a general-purpose AI chatbot that answers money questions is not. Whether «AI financial advice» is regulated, according to the SEC, depends less on the technology and more on what the tool actually does — and who, if anyone, stands behind it.

This guide explains, in plain terms, how U.S. rules treat AI in financial advice — the Investment Advisers Act of 1940, fiduciary duty, and the separate roles of the SEC and FINRA — and shows you how to verify for yourself whether the «advisor» you’re using is an actual regulated professional. It’s educational context only; see the disclaimer above.

Are AI Financial Advisors Regulated? The Short Answer

It depends on function, not the word «AI»

As of mid-2026, the SEC has not enacted AI-specific rules for investment advisers. Instead, U.S. regulators apply existing law — chiefly the Investment Advisers Act of 1940 — to whatever the tool actually does, regardless of how it was built. Regulation follows the function a tool performs, not its branding:

- Personalized investment advice for compensation — treated as adviser activity, subject to the Investment Advisers Act.

- General financial education, with no personalized securities recommendations — generally not treated as adviser activity.

- Executing trades on a user’s behalf — may fall under separate broker-dealer rules, not just adviser rules.

That distinction matters more than most marketing copy admits. An «AI investment advisor» and an «AI money advisor» can describe two very different products — one built by a registered firm, the other a general-purpose chatbot with no registration at all. The label doesn’t tell you which one you’re using; the underlying registration does.

«Regulated» means a person or firm is registered — not the algorithm

The law regulates the adviser — a person or firm — not the software itself. A robo-advisor is regulated because a registered firm stands behind it, files paperwork, and answers to examiners. A free chatbot is not regulated as an adviser, because no registered fiduciary stands behind its output. This single point resolves most of the confusion around «AI financial advisor tool» marketing: ask who is registered, not what technology is running underneath.

The practical upshot is that two products can use identical underlying AI models and still sit on opposite sides of the regulatory line — the deciding factor is whether a registered adviser has taken legal responsibility for the output.

The Law Behind It: The Investment Advisers Act of 1940

What counts as an «investment adviser»

The Investment Advisers Act of 1940 defines an investment adviser as anyone who, for compensation, is in the business of advising others about the value of securities or the advisability of buying or selling them. That «for compensation» and «advising about securities» test is what pulls a tool — human or automated — into the regulatory regime. A general chatbot that discusses budgeting concepts without personalized securities recommendations typically sits outside that definition; a paid service that tells you which specific investments to buy does not.

This is why two apps that look similar on the surface can be treated very differently under the law — one charges a fee for tailored buy-or-sell recommendations, while the other only explains general concepts like diversification or compound interest.

Registration and Form ADV

Advisers register with the SEC, or with state regulators, by filing Form ADV through the IARD system. As a general threshold, a mid-sized adviser must register with the SEC once its regulatory assets under management reach $110 million; advisers below that level usually register with their state instead. Form ADV is public, and it discloses:

- The firm’s fees and compensation structure.

- Business practices, including any conflicts of interest.

- Disciplinary history, if any exists.

- Ownership and the individuals who manage client accounts.

| Adviser size (regulatory AUM) | Typical registration | Files Form ADV |

|---|---|---|

| Below $110 million | State securities regulator | Yes |

| $110 million and above | SEC | Yes |

| No registration at all | Not a registered adviser | No |

Fiduciary Duty: The Line That Separates a Licensed Advisor From a Chatbot

A registered investment adviser owes a fiduciary duty — a duty of care and a duty of loyalty — meaning it must act in the client’s best interest at all times and cannot put its own interests first. This duty cannot be delegated to an algorithm; the registered firm remains accountable for what the algorithm recommends.

A general-purpose AI chatbot is not a fiduciary. This is the key differentiator to understand before trusting any AI tool with money questions: a general-purpose AI or large language model chatbot has no fiduciary duty, no license, and no regulatory oversight of its «advice.» If its output leads to a financial loss, there is typically no adviser-client legal recourse the way there would be with a registered firm. Independent testing backs this up: one widely cited test of 100 finance-related questions found a general-purpose chatbot gave wrong or misleading answers roughly 35% of the time — a reminder to treat AI output as a starting point for research, not a final answer.

As the Investor.gov guidance on checking investment professionals puts it plainly:

Unlicensed, unregistered persons commit much of the investment fraud in the United States.

Investor.gov

That warning applies just as much to an unregistered AI tool as it does to an unregistered human — the format of the «advisor» doesn’t change the risk.

Robo-Advisors vs. General AI Chatbots: Two Very Different Things

Robo-advisors: algorithms inside a registered firm

A robo-advisor — the automated portfolio service many brokerages now offer — is typically a Registered Investment Adviser: it files Form ADV, is subject to examination, and owes fiduciary duty just like a human adviser firm. Automation doesn’t remove those obligations; it just changes who (or what) executes the day-to-day portfolio decisions. According to the FINRA Investor Alert on automated investment tools, automated tools rely on assumptions that may not reflect current market conditions, may present a limited set of investment options, and their output depends heavily on the information you feed them.

That last point is worth sitting with: a robo-advisor’s recommendation is only as good as the risk tolerance and goals you entered into the questionnaire, so inaccurate inputs can lead to a mismatched portfolio even inside a fully regulated product.

General AI chatbots: helpful for learning, not a regulated advisor

An AI financial assistant or general-purpose chatbot can be genuinely useful for explaining concepts, brainstorming budgeting ideas, and organizing questions to bring to a licensed professional. But it is not a registered adviser and holds no fiduciary duty toward you. Used this way — as a research and education tool rather than a decision-maker — an artificial intelligence financial advisor tool can add real value without pretending to be something it isn’t.

The safest pattern is to treat the chatbot as a first draft: let it help you frame the question, then take that question to a source that is actually accountable for the answer.

| Robo-advisor | General AI chatbot | |

|---|---|---|

| Registered with SEC/state | Usually yes | No |

| Fiduciary duty | Yes | No |

| Files Form ADV | Yes | No |

| Best use | Managing an actual portfolio | Learning concepts, organizing questions |

What «SEC-Regulated AI Advisor» Claims Really Mean

The registered firm is regulated — read the claim carefully

A phrase like «SEC-regulated AI advisor» usually means the firm offering the tool is a registered investment adviser — the SEC regulates the firm, not the AI model itself. That distinction is meaningful, but it is not the same as the AI being independently «approved» or «certified» by the SEC; regulators do not endorse or certify specific products, AI-based or otherwise.

Marketing language often blurs this line on purpose, borrowing the credibility of «SEC-regulated» without spelling out that the regulation applies to the business, not to the model generating the text.

Regulators are watching AI claims

In March 2024, the SEC settled charges against two advisers, Delphia and Global Predictions, for false and misleading statements about their use of artificial intelligence — a practice now commonly called «AI-washing» — with penalties of $225,000 and $175,000, respectively, totaling $400,000. The SEC’s 2026 Examination Priorities include AI policies and disclosures, signaling that scrutiny of AI marketing claims in the advisory industry is continuing rather than fading.

Before trusting a claim like this, it helps to ask a few direct questions:

- Is the firm — not just the app or the model — actually registered with the SEC or a state regulator?

- Can you find that registration independently on IAPD, rather than taking the firm’s word for it?

- Does the claim describe the firm’s regulatory status, or does it imply the SEC «approved» the AI itself?

FINRA, the SEC, and CFPB: Who Oversees What

The SEC oversees investment advisers; FINRA is a self-regulatory organization that oversees broker-dealers and their registered representatives; and the CFPB focuses on consumer financial products more broadly, such as credit and lending. A single tool can touch more than one of these regimes depending on what it actually does — advising on securities, executing trades, or offering consumer credit products.

- SEC — registers and examines investment advisers under the Investment Advisers Act of 1940.

- FINRA — a self-regulatory organization overseeing broker-dealers and registered representatives.

- CFPB — focuses on consumer financial products, separate from securities advice.

- State regulators — register smaller advisers below the SEC’s asset threshold.

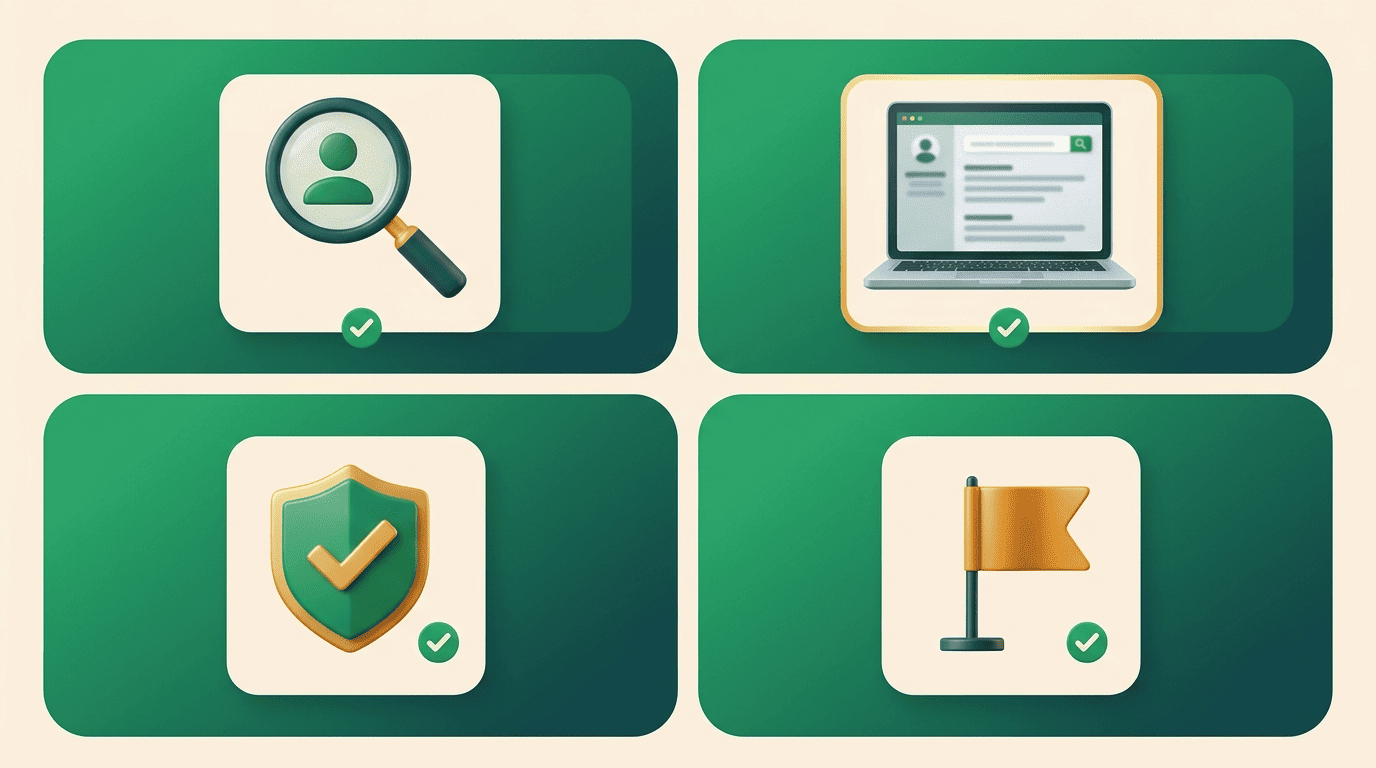

How to Verify an Advisor Yourself (Step by Step)

- Search the firm or individual’s name at Investor.gov — it routes you to the right database.

- On the Investment Adviser Public Disclosure system (adviserinfo.sec.gov), confirm SEC or state registration and read the firm’s Form ADV.

- Check FINRA BrokerCheck (brokercheck.finra.org) for brokers and any disciplinary history.

- Confirm that the tool or firm itself — not just «the AI» — is the party actually registered.

- If no one can be found in either database, treat it as a red flag: unlicensed, unregistered persons commit much of the investment fraud in the United States.

For direct questions, the SEC can be reached at (800) 732-0330 and FINRA at 301-590-6500.

FAQ

Reminder: everything above is educational information only, not financial advice, and not a substitute for a licensed financial advisor. Use an AI tool to learn and organize your questions — then bring the decisions that matter to a licensed professional.