AI Financial Advisor vs Human Advisor: What Each Does Best (and When to Use Which)

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

A good AI financial advisor can crunch your budget, model retirement scenarios, and answer money questions at 2 a.m. — but it is not the same thing as a licensed human advisor who is legally on the hook for your interests. This guide compares an AI-powered financial advisor with a human, fiduciary advisor: where each is strong, where each falls short, and why most people are best served by using both.

AI advisor, robo-advisor, human advisor: what’s the difference?

An AI financial advisor is a software tool that uses large language models and algorithms to answer money questions, categorize spending, and explain concepts. A robo-advisor is a related but narrower category: the SEC defines a robo-adviser as «an automated digital investment advisory program» that collects your goals, time horizon, income, and risk tolerance through an online questionnaire and then builds and manages a portfolio, «sometimes with little or no interaction with a human being,» according to the Investor.gov robo-adviser bulletin.

A human financial advisor is a licensed person — often a CFP® professional or someone at a Registered Investment Adviser (RIA) firm — who gives personalized advice and, in many cases, manages money on your behalf.

In practice, the three terms cover overlapping but distinct ground:

- AI financial advisor — a broad label for any AI-driven tool that answers money questions, from a general chatbot to a dedicated planning app.

- Robo-advisor — a narrower, regulated category: an automated program that builds and manages an actual investment portfolio.

- Human advisor — a licensed individual or firm, sometimes a CFP® professional, who advises and may manage money directly.

The table below lays out the basic distinctions among the three.

| AI financial advisor (general tool) | Robo-advisor | Human advisor | |

|---|---|---|---|

| What it is | Chatbot / planning software | Automated investment program | Licensed individual or firm |

| Registration | Not necessarily registered | Registers as investment adviser | Registers as investment adviser / RIA |

| Human contact | None or minimal | Little or none | Direct, ongoing |

| Typical use | Education, budgeting, questions | Portfolio building and rebalancing | Complex planning, judgment calls |

Fiduciary duty: the biggest difference of all

The CFP Board describes a fiduciary as «a financial advisor legally required to act in your best interests,» who must prioritize your needs and disclose conflicts of interest, per its fiduciary vs. financial advisor explainer. CFP® professionals are held to this fiduciary standard; some other advisors operate under a lower «suitability» or best-interest standard that can permit commission-earning recommendations.

Where AI sits legally

In the U.S., a robo-advisor is regulated as an investment adviser — it must register with the SEC or a state, file Form ADV, and owes fiduciary and anti-fraud duties. But a general-purpose AI chatbot that is not a registered adviser makes no such promise and answers to no one for your outcome. Accountability — a named professional who can be held responsible — is the line an AI-powered financial advisor has not crossed.

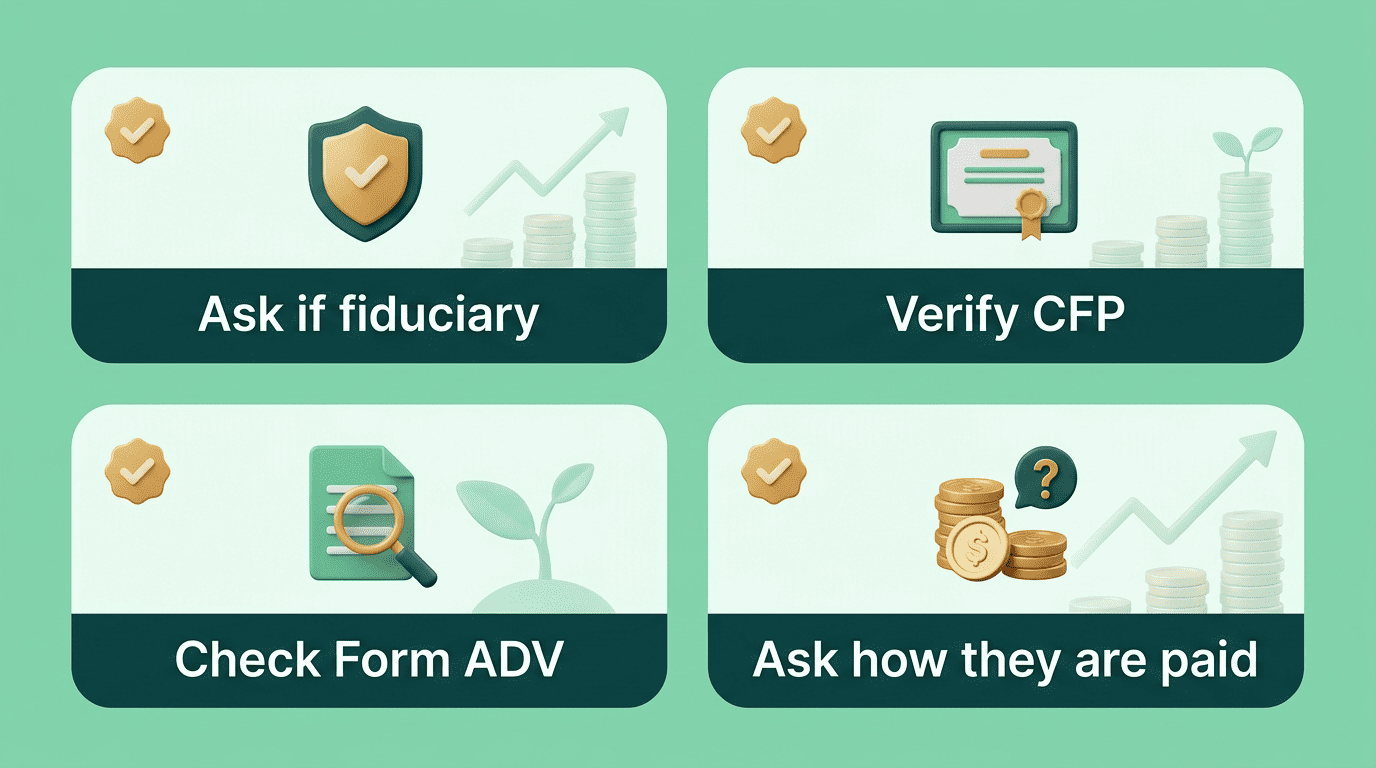

Before trusting any adviser with your money, it helps to know what to check first:

- Ask the person or firm directly whether they act as a fiduciary at all times.

- Request the fiduciary commitment in writing, not just verbally.

- Confirm CFP® certification status with the CFP Board if they claim it.

- Look up the firm’s Form ADV and registration on Investor.gov.

- Search the disciplinary history section of the same filing.

- Ask how the advisor (or firm behind the AI tool) is compensated.

- Repeat the same checks for a robo-advisor or AI tool that manages actual investments, not just one that answers questions.

What an AI financial advisor does well

An AI-powered financial advisor tool is fast, available 24/7, and tireless. It can summarize a portfolio, run retirement or Monte Carlo–style projections, build a budget, and explain the difference between a Roth and traditional account in plain language — instantly and usually at low or no cost.

Speed and constant availability. An AI-driven financial advice tool doesn’t keep office hours. It can answer a question about an emergency fund at midnight or walk through a budgeting scenario on a Sunday, something a human advisor’s calendar rarely allows.

Organizing the numbers. Categorizing transactions, tracking net worth, and building a first-draft budget are exactly the kind of repetitive, data-heavy tasks an automated financial advisor handles efficiently.

Education and preparation. This is where AI shines for most people: learning the vocabulary, organizing numbers, and walking into a meeting with a human advisor already prepared with the right questions.

What a human advisor does that AI can’t

A human advisor can sit with you through a market crash, a job loss, a divorce, or the death of a spouse and help you avoid a costly emotional decision. FINRA warns that automated tools rely on «assumptions that could be incorrect or do not apply to your individual situation» and may overlook your age, full financial picture, tax situation, and risk tolerance, according to its guidance on automated investment tools.

Judgment in complex, emotional moments

Behavioral coaching — talking a client out of selling everything during a downturn, or into staying the course through a scary headline — is a role built on trust and repeated human contact, not a single chatbot exchange.

Complex taxes, estates, and coordination

For business owners, blended families, concentrated stock, or estate planning, a human coordinates across tax, legal, and investment decisions in ways a single tool typically cannot — and takes responsibility for the recommendation. Situations that typically call for a human advisor rather than a tool alone include:

- Selling a business or a large concentrated stock position

- Coordinating estate planning across multiple family members

- Navigating divorce, inheritance, or a sudden change in income

- Combining tax, legal, and investment decisions that interact with each other

As one industry body puts it:

An automated tool may rely on assumptions that could be incorrect or do not apply to your individual situation.

FINRA

That warning applies just as much to a general AI financial advisor tool as it does to a robo-advisor, since both work only with the information and assumptions they’re given.

Cost: what you actually pay

The SEC notes robo-advisers generally carry «lower costs and fees than traditional advisory programs, and in some cases require lower account minimums,» per the same Investor.gov robo-adviser bulletin. A human advisor typically costs more, reflecting personalized, accountable advice. Confirm any specific fee figures directly with the provider — fee structures vary by firm and are not promised here.

| Factor | AI financial advisor / robo-advisor | Human financial advisor |

|---|---|---|

| Typical cost level | Generally lower | Generally higher |

| Account minimums | Often lower or none | Can be higher |

| What you’re paying for | Software, automation, self-service tools | Personalized judgment, accountability, coordination |

| Fee transparency | Confirm directly with the provider | Confirm directly with the firm / Form ADV |

Is an AI financial advisor safe to use?

For any adviser — AI-driven or human — the SEC recommends checking registration, license status, and disciplinary history through the Investment Adviser Public Disclosure (IAPD) database, described in the Investor.gov robo-adviser bulletin. Remember that an AI tool’s output is only as good as the information you give it, and the SEC cautions that in some cases robo-advisers «may not have been tested under stressed market conditions.»

A few habits reduce risk when using any digital financial advisor tool:

- Treat AI output as a starting point for questions, not a final decision.

- Never share account passwords or full account numbers in a chat window.

- Cross-check any registered adviser’s status on the SEC’s IAPD database.

- Re-verify important numbers (balances, tax figures) against your actual statements.

The bottom line: use AI to prepare, a human to decide

Most people don’t have to choose. Use an AI financial advisor tool to learn, budget, organize your numbers, and prepare good questions — then bring a licensed, fiduciary human advisor in for the decisions that carry real money, tax, and emotional weight. An AI-driven financial advice tool works well as the first stop, not the last one.