AI Financial Advisor vs. Robo-Advisor: What’s the Real Difference?

«AI financial advisor» and «robo-advisor» sound almost interchangeable, but they describe two different tools. Today, an AI financial advisor usually refers to a conversational AI assistant that explains money concepts and answers questions, according to the SEC’s Investor Bulletin on robo-advisers, while a robo-advisor is an automated service that actually holds and manages your investment portfolio.

The core difference fits in one sentence: a robo-advisor manages your money and is usually registered as a fiduciary, while a conversational AI assistant teaches and helps you plan, but never touches your accounts.

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

The Short Answer: Two Different Tools

A robo-advisor is an automated portfolio manager: it holds your brokerage account, buys and sells securities, and rebalances your holdings on a schedule. An AI financial advisor, in the newer conversational sense, is an LLM-based assistant that answers questions about budgeting, debt, and basic investing concepts — but it has no access to your money and generally does not carry a fiduciary duty toward you. The distinction matters because the two get lumped together in casual conversation, yet the SEC and FINRA treat them very differently for regulatory purposes.

Quick comparison table

| Robo-advisor | AI financial advisor (assistant) | |

|---|---|---|

| Manages your money | Yes | No |

| Registered as RIA | Usually | Usually not |

| Fiduciary duty | Yes, as an RIA | Generally no |

| What it does | Allocates, rebalances, tax-loss harvests | Educates, explains, models scenarios |

| Typical cost | ~0.25%–0.50% AUM/year, some $0 | Flat subscription or free |

| Human in the loop | Limited or none, unless hybrid | Limited or none, unless hybrid |

What a Robo-Advisor Actually Is

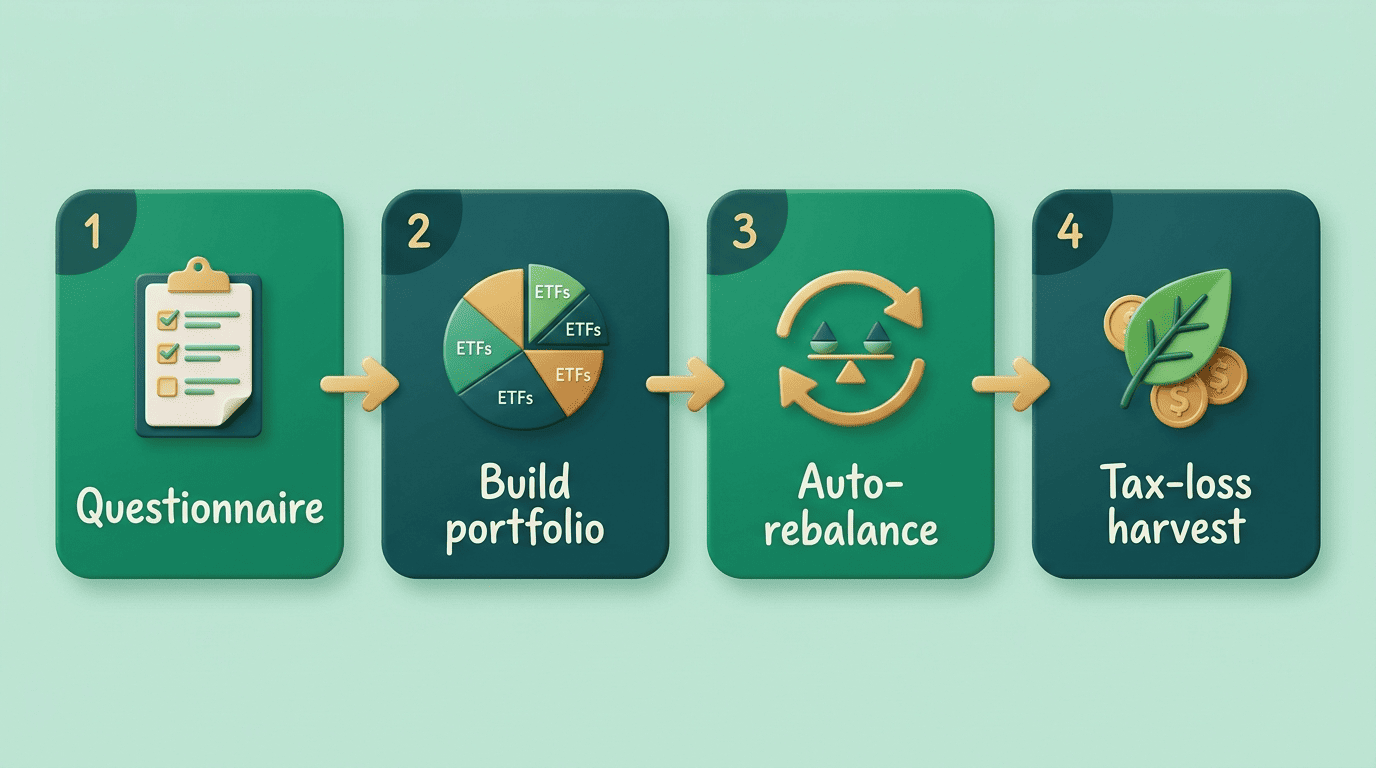

A robo-advisor exists to take the manual work out of investing. Instead of you researching individual stocks, an algorithm builds and maintains a diversified portfolio on your behalf, based on the answers you give during onboarding.

How a robo-advisor works

You start with an onboarding questionnaire covering age, time horizon, and risk tolerance. From those answers, the algorithm builds a diversified portfolio of low-cost ETFs grounded in Modern Portfolio Theory, the framework developed by economist Harry Markowitz.

Once the portfolio is built, the automated portfolio manager runs several tasks on an ongoing basis, without you having to log in and place trades yourself:

- Rebalances the portfolio automatically whenever an allocation drifts past its target

- Reinvests dividends as they’re paid out

- Applies tax-loss harvesting to offset gains, on providers that support it

- Adjusts the allocation over time as you approach a stated goal or retirement date

Betterment, founded in 2008 and launched in 2010, is widely credited as the first robo-advisor; Wealthfront followed in 2011, and Vanguard later added its own Vanguard Digital Advisor to the category.

What robo-advisors are good at (and their limits)

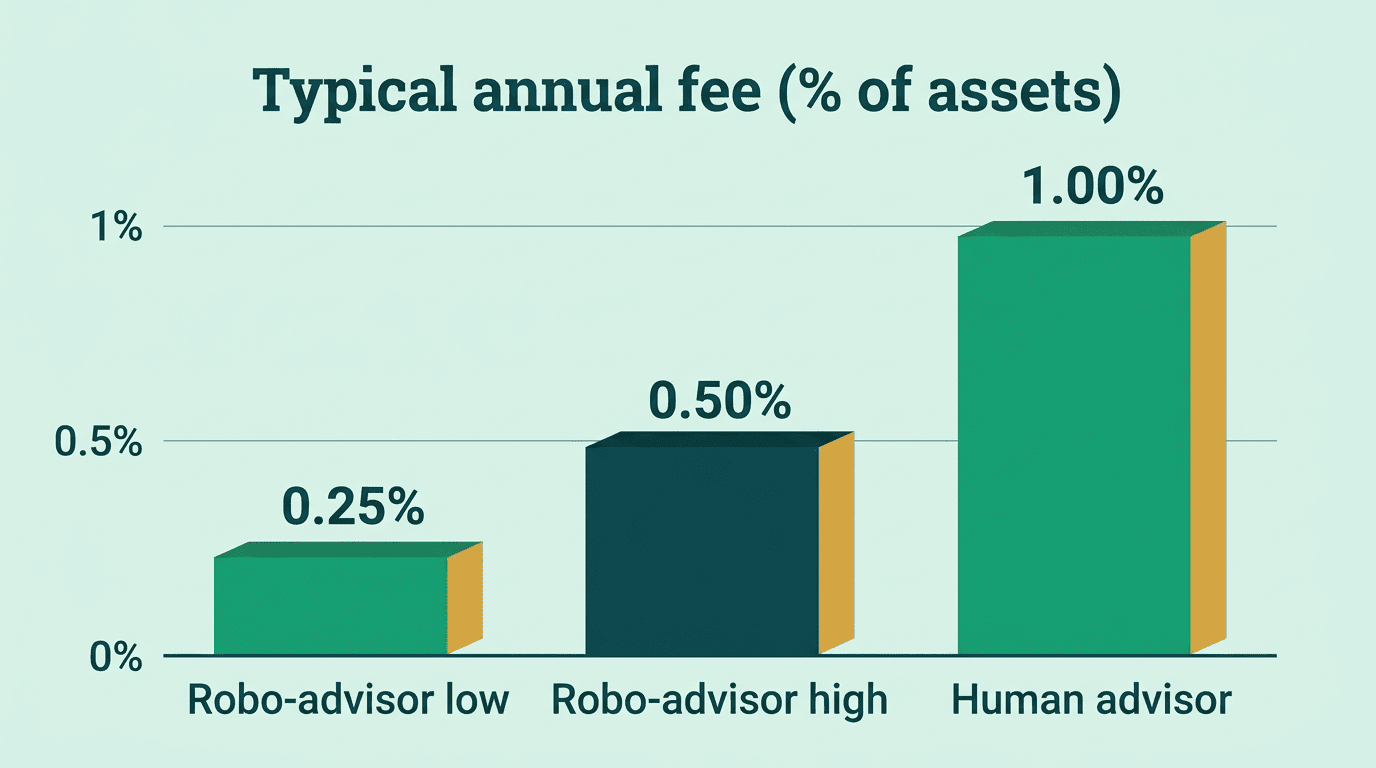

Robo-advisors are strong at low-cost, disciplined, hands-off investing. Fees typically run around 0.25%–0.50% of assets under management per year — roughly $125 to $250 annually on a $50,000 balance — and some providers charge $0. That compares favorably to a human advisor, who typically charges closer to 1% AUM. Minimums are often low or nonexistent, which makes robo-advisors accessible to new investors.

The limits are just as real. The SEC’s investor bulletin notes that a robo-advisor’s recommendation is generally only as good as the short online questionnaire behind it, and most robo-advisors focus narrowly on investment management rather than comprehensive financial planning. Customization tends to be limited, and a robo-advisor typically has no view into the rest of your financial life — your home, taxes, or estate plans.

What an AI Financial Advisor (LLM Assistant) Actually Is

An AI financial advisor, or AI-powered financial advisor, is a different category of tool built on a large language model such as GPT, Claude, or Gemini. Rather than holding assets, it holds a conversation.

What it does well

An AI financial advisor tool explains financial concepts in plain language, answers questions like «what is an ETF» or «should I pay off debt early,» and can model «what if» scenarios on request. It also helps with everyday budgeting and goal planning, and it’s typically available around the clock, often for free or a modest subscription.

In practice, that usually shows up as help with:

- Explaining unfamiliar terms — ETF, expense ratio, AUM fee — in plain language

- Walking through «what if» scenarios, like paying off debt faster versus investing more

- Building a basic budget or savings plan around a stated goal

- Preparing questions to bring to a human financial planner

Throughout, the user stays in control — the assistant offers information and options, but the person makes every decision about their own money.

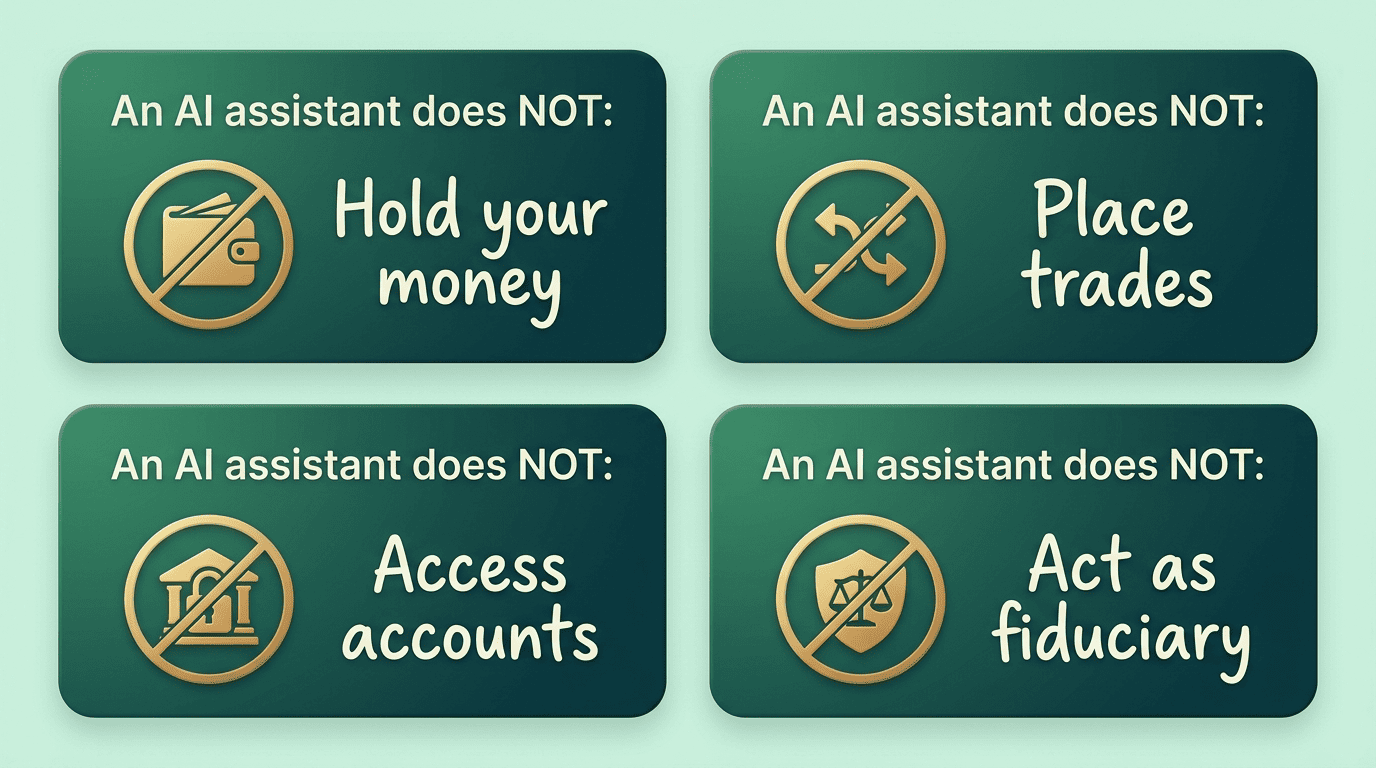

What it does NOT do (critical)

This is where the two tools diverge sharply. Compared with a robo-advisor, a conversational AI financial advisor:

- Generally does not hold or manage your money

- Does not execute trades on your behalf

- Has no direct access to your brokerage or bank accounts

- Is typically not a registered investment adviser

- Generally does not owe you a fiduciary duty

It can also be wrong — language models can produce inaccurate or outdated information, and an AI assistant doesn’t know your complete financial picture unless you disclose it in the conversation. That’s why these tools are best treated as education, not as a source of personalized recommendations to buy specific securities.

«Robo» Doesn’t Mean «AI»: Clearing Up the Confusion

One of the most common mix-ups is assuming «robo-advisor» means the same thing as «AI.» Despite the name, most robo-advisors run on deterministic, rule-based algorithms — for example, triggering a rebalance whenever an allocation drifts past a set threshold — rather than on machine learning or language models. «Robo» describes automation, not intelligence. A newer wave of tools layers a conversational LLM interface on top of or alongside traditional robo-advisor infrastructure, but that combination is really its own category, distinct from either a classic robo-advisor or a pure AI-powered financial advisor.

Side-by-Side: Money, Regulation, Cost, Personalization

Beyond the basic «who touches the money» question, robo-advisors and AI assistants also differ in how they’re regulated and what they cost.

Who manages the money

A robo-advisor operates on a discretionary basis: it actually holds and manages your portfolio, executing trades without asking permission each time. An AI-powered financial advisor never touches your money — it only produces text on a screen in response to your questions.

That single distinction — custody of assets — is what separates the two categories legally and practically. Once a service takes discretionary control of your investments, it steps into a different regulatory bucket than a tool that simply answers questions.

Regulation and fiduciary duty

According to the SEC’s Investor Bulletin: Robo-Advisers, robo-advisors operating in the United States are generally registered as Registered Investment Advisers (RIAs), subject to the same securities laws as traditional advisers, and required to file a Form ADV. As registered investment advisers, they owe clients a fiduciary duty — an obligation to act in the client’s best interest. A conversational AI financial advisor, by contrast, is typically not registered as an investment adviser and generally does not owe that same fiduciary duty.

Robo-advisors or robo-advisers are financial advisers that provide personalized financial advice and investment management online with moderate to minimal human intervention.

Wikipedia, Robo-advisor

That definition explains why the fiduciary standard applies to robo-advisors in the first place: they are registered financial advisers, just automated ones. A conversational AI assistant, by contrast, generally isn’t registered as a financial adviser at all, so that same legal obligation generally doesn’t apply to it.

A robo-advisor’s Form ADV, filed with the SEC, typically discloses:

- Its fee schedule and any additional costs

- The investment strategy and methodology behind its portfolios

- Any conflicts of interest between the firm and its clients

- Disciplinary history, if any

Cost

A robo-advisor typically costs around 0.25%–0.50% of assets under management per year, with some providers charging nothing, plus the underlying expense ratios of the ETFs it holds. A human financial advisor tends to run closer to 1% AUM. An AI financial advisor tool is usually free or available on a flat subscription — but remember, it isn’t managing any assets in exchange for that fee.

The two pricing models aren’t measuring the same thing, which makes a side-by-side comparison useful:

| Robo-advisor | AI financial advisor (assistant) | |

|---|---|---|

| Pricing model | Percentage of AUM per year | Flat monthly subscription or free |

| Registered under | SEC as an RIA (files Form ADV) | Generally not registered as an adviser |

| Underlying costs | ETF expense ratios, on top of the AUM fee | None — no assets held |

| Typical minimum | $0–$500 depending on provider | None |

| Where to verify | SEC IAPD database via Investor.gov | Provider’s own disclosures |

When Each One Fits — and Using Both Together

Neither tool is a universal answer. The right choice depends on what you’re actually trying to solve.

- Decide what you need first. If the goal is ongoing investment management, a robo-advisor is built for that. If the goal is understanding a concept or thinking through a decision, an AI assistant fits better.

- Check your risk tolerance and time horizon. These inputs shape a robo-advisor’s portfolio recommendation, so have honest answers ready before you sign up.

- Ask what the AI assistant discloses about itself. A trustworthy AI financial advisor tool should be upfront that it isn’t a licensed adviser and isn’t managing your money.

- Compare fees side by side. Look at AUM percentage for a robo-advisor versus subscription cost for an AI assistant — they aren’t measuring the same service.

- Verify any registered adviser’s status. Before opening an account with a robo-advisor or human RIA, look them up in the SEC’s IAPD database via Investor.gov.

- Use both if it makes sense. Many people lean on an AI assistant to learn and plan, then let a robo-advisor handle the mechanical work of investing.

- Escalate to a human for complex situations. Tax optimization, estate planning, and large sums warrant a licensed, fiduciary financial planner.

Choose a robo-advisor if…

You want an inexpensive, disciplined, largely hands-off way to invest — a diversified ETF portfolio, automatic rebalancing, and tax-loss harvesting — without making day-to-day allocation decisions yourself.

This fits well if your main goal is long-term investing rather than active trading or complex financial planning, and you’re comfortable handing execution over to an algorithm within the parameters you set during onboarding.

Choose an AI assistant if…

You want to understand basic concepts, ask questions about budgeting, debt, or goals, model different scenarios, or prepare for a conversation with a human advisor, all while keeping full control over your own money.

This fits well when you’re still learning or deciding what to do, rather than ready to hand off investment management to an automated service — the AI assistant informs the decision, but you’re the one who acts on it.

Use both — and know when to call a human

Many people combine the two: a conversational assistant as a co-pilot for learning and planning, paired with a robo-advisor as the «autopilot» that actually executes trades. For complex, high-stakes questions — tax strategy, estate planning, large windfalls, major life events — the safer path is a licensed, fiduciary financial planner such as a CFP. Before working with any adviser, robo or human, check their registration and disciplinary history in the SEC’s IAPD database at Investor.gov.

Robo-advisors and conversational AI tools both have a place in a modern financial toolkit, but neither one replaces professional judgment for decisions that carry real financial weight — an AI financial advisor tool is best used as a starting point for education, not as the final word.

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.