Best AI Financial Advisor Tools in 2026: A Category-by-Category Comparison

«AI money tools» is now an umbrella term for three very different families of software, and picking an AI financial advisor is really about matching a tool to a specific job, not finding a single winner. According to Investor.gov, the SEC’s investor-education site, some of these tools are registered investment advisers with legal duties attached, while others are just chat interfaces with no such obligation. This guide compares the categories factually — general-purpose LLM assistants, dedicated AI finance apps, and robo-advisors — so you can match a tool to your job rather than chase a «best» label that doesn’t really apply here.

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions. Note that 47% of consumers already use or consider AI chatbots for money management, per an Experian survey from October 2024 — but adoption is not the same as suitability, and the gap between the two is most of what this article is about.

The Three Categories of AI Financial Tools

Nearly every AI money tool on the market falls into one of three buckets, and confusing them is the single most common mistake people make when they go looking for help with their finances. A general LLM assistant is a type of AI financial tool, but it is a broad, conversational one — it was not built for money specifically. A robo-advisor sits at the other end: it is registered as an SEC investment adviser and carries a fiduciary duty, a legal standard that requires it to act in your best interest. A general LLM assistant, by contrast, lacks that fiduciary duty entirely, no matter how confidently it answers a question about your 401(k).

| Category | Examples | Manages money? | Fiduciary duty? |

|---|---|---|---|

| General-purpose AI assistant | ChatGPT, Google Gemini, Microsoft Copilot, Claude | No | No |

| Dedicated AI finance app | Origin, Cleo, Rocket Money, YNAB | Sometimes tracks/moves money via linked accounts | Varies — check disclosures |

| Robo-advisor | Betterment, Wealthfront | Yes — builds and rebalances a portfolio | Yes, if SEC-registered |

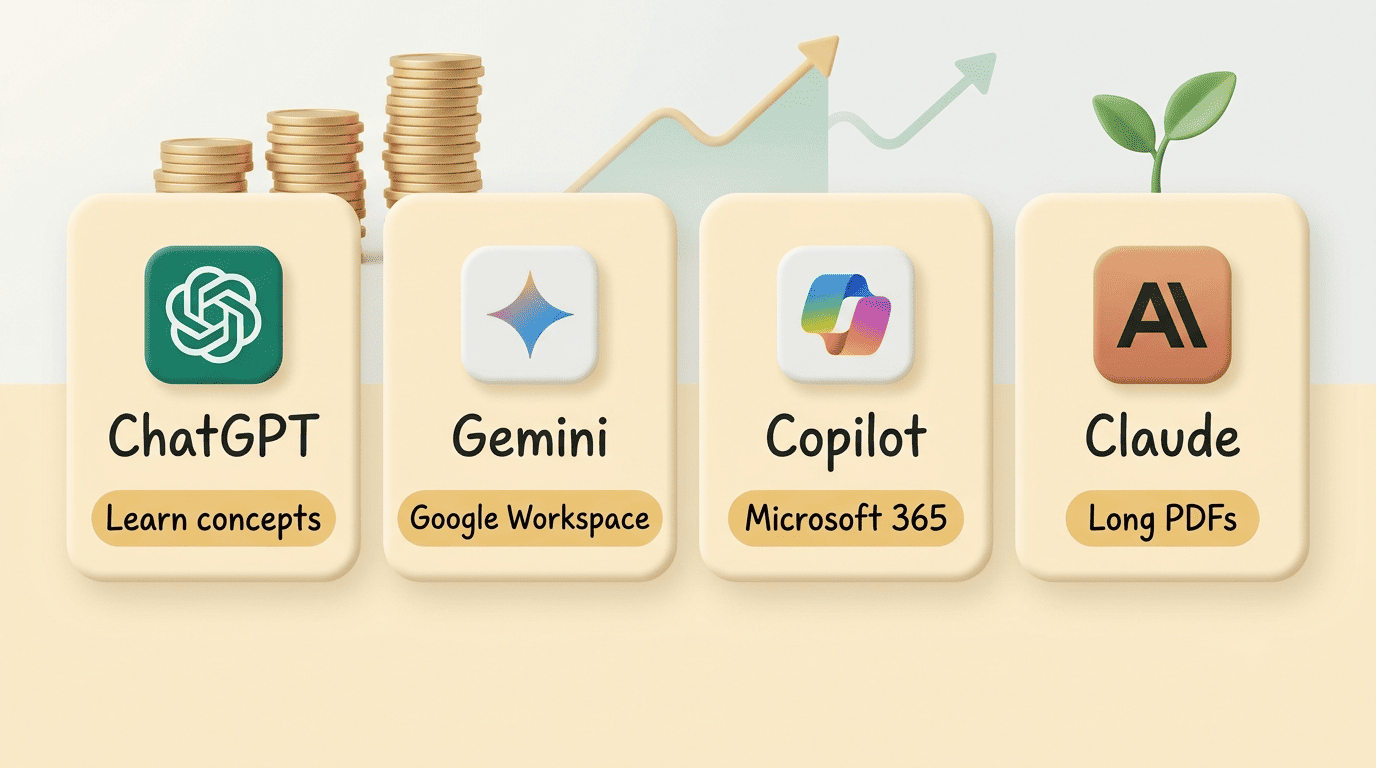

General-purpose AI assistants

ChatGPT, Google Gemini, Microsoft Copilot, and Claude are conversational LLMs that explain concepts, draft budgets, and compare options in plain language. Wealth Enhancement Group’s own framing of these four tools is useful: ChatGPT for learning concepts, Gemini for people already living inside Google Workspace, Copilot for anyone working inside Microsoft 365, and Claude for reading and summarizing long PDFs like a prospectus or a loan agreement. The key limit across all four is the same — none of them has access to your live accounts, none carries a fiduciary duty, and any of them can hallucinate a fact that sounds entirely plausible.

Dedicated AI finance apps

Origin, Cleo, Rocket Money, Monarch Money, Copilot Money, YNAB, and Empower are purpose-built for budgeting, subscription tracking, and cash-flow visibility. Most connect directly to your bank accounts, often through Plaid, and layer AI on top of your real transactions rather than a hypothetical scenario you typed in. A few, like Origin, market advisor-grade features and cite internal benchmarks — treat those as vendor marketing, not independent proof, and verify any specific claim on the company’s own site before relying on it.

Robo-advisors

Betterment, Wealthfront, and Schwab Intelligent Portfolios are automated portfolio managers registered with the SEC as investment advisers, which means they owe a fiduciary duty to the client. Per Investor.gov, robo-advisers typically build a portfolio from your stated goals and risk tolerance, then use algorithms — often grounded in Modern Portfolio Theory — to rebalance it and apply tax-loss harvesting. They do genuinely manage money, but on a narrow set of inputs; a robo-advisor does not see your whole financial picture the way a human fiduciary advisor might.

General-Purpose LLM Assistants: Strengths and Limits

The four mainstream assistants — ChatGPT, Gemini, Copilot, and Claude — are strongest when the job is understanding something, not deciding something. That distinction matters more than which vendor’s model happens to be ahead this quarter, because the underlying limitation (no fiduciary duty, no live account access) is structural, not a feature gap that a future update will close.

What they are good at

Explaining jargon in plain language. A general LLM assistant is genuinely useful for a specific, bounded set of tasks:

- Explaining the difference between a Roth and a Traditional IRA, or the 50/30/20 budgeting rule

- Comparing the debt snowball method against the debt avalanche method

- Drafting a starter budget from numbers you supply

- Generating a list of questions to bring to a human advisor before a real meeting

MIT Sloan’s coverage of generative AI in financial planning, featuring MIT Sloan finance professor Andrew Lo, notes that these tools can help people frame financial decisions and build financial literacy — used as a collaborative partner for explaining trade-offs and exploring scenarios, not as an oracle — which is a genuinely useful function even without any account access. In short, they are strong for education, not execution — a distinction worth keeping in mind before you ask one to manage anything real.

Where they fall short

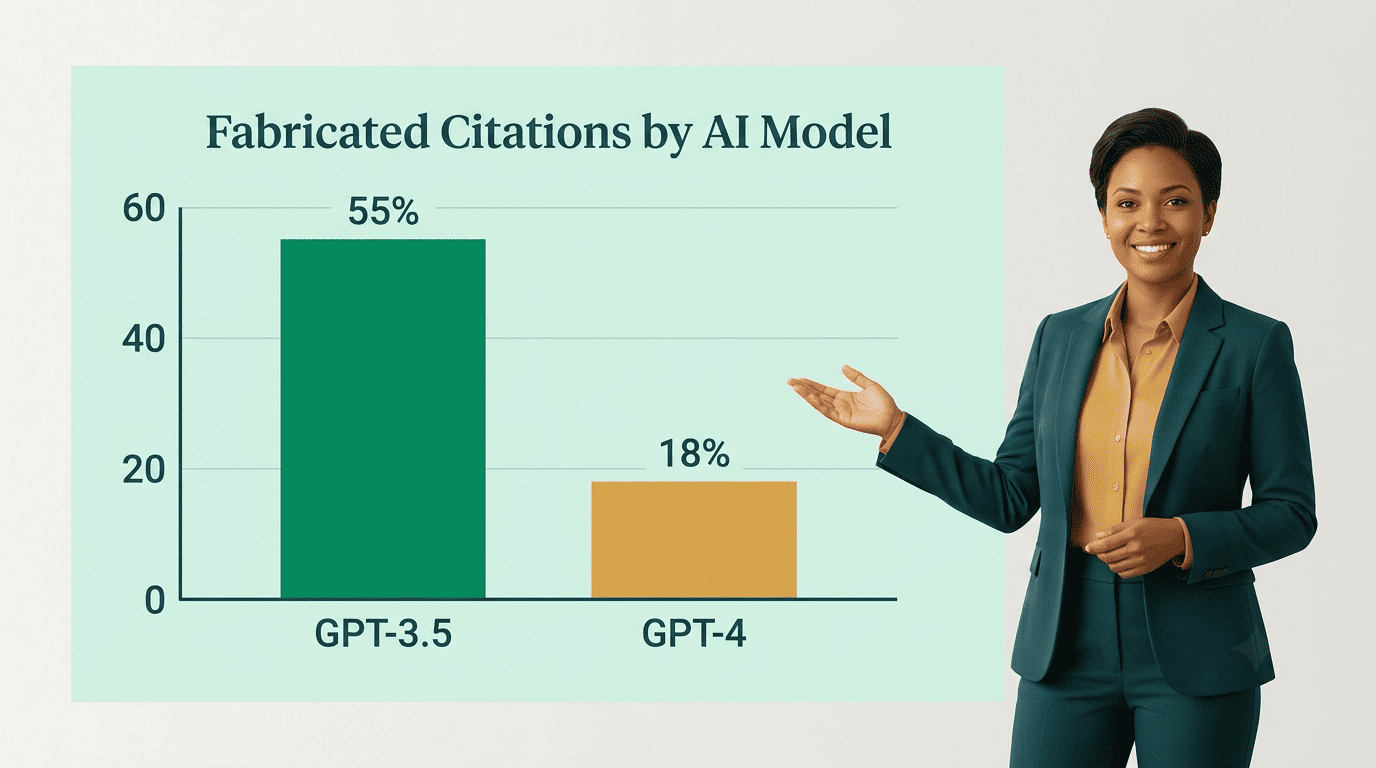

A general-purpose AI financial advisor tool has no fiduciary duty to you, full stop — nothing legally obligates it to act in your interest over anyone else’s. Hallucination is a documented, real risk: a peer-reviewed study published in Scientific Reports found that 55% of the bibliographic citations ChatGPT-3.5 produced were fabricated outright — invented papers and author names presented with total confidence, versus 18% for GPT-4 — a reminder that any factual claim needs independent verification, not just a confident tone. There are also possible undisclosed conflicts worth weighing — Microsoft has invested roughly $13 billion in OpenAI, so a Copilot or ChatGPT recommendation that happens to favor Microsoft products deserves a second look. None of these assistants can see your live accounts unless you paste the data in yourself, which creates its own privacy risk. Always verify any number an assistant gives you against an independent, official source.

Dedicated AI Finance Apps: What They Actually Do

Unlike a chat window, these apps are built around a live feed of your actual transactions, which is both their main advantage and the reason data-sharing questions matter more here than with a general assistant.

Budgeting and cash-flow assistants

Cleo, Rocket Money, Monarch Money, Copilot Money, and YNAB all connect to your accounts, categorize spending automatically, flag recurring subscriptions, and send nudges when you’re off track. Rocket Money, for instance, scans transactions to find recurring charges; its concierge can cancel unwanted subscriptions at no extra cost, while its separate bill-negotiation service takes a cut of whatever it saves you in the first year if it succeeds in lowering a bill — check current terms directly with the provider rather than trusting a secondhand figure. Pricing across this category changes often; this article does not quote live prices as fact, so confirm the current tier and cost on the official app before subscribing. The Consumer Financial Protection Bureau has separately cautioned that finance chatbots embedded in these apps can sometimes give inaccurate or unhelpful answers, which is worth keeping in mind even when the app is otherwise well built.

«Advisor-grade» AI platforms

A smaller group of apps, Origin among them, market themselves as delivering «advisor-grade» AI and point to internal benchmarks — sometimes framed as CFP-exam-style scores — to back that claim. Treat a vendor’s self-administered test as marketing material, not independent proof, the same way you would treat any other in-house benchmark. Before trusting the advisory output, check whether it is actually delivered through an SEC-registered RIA (registered investment adviser) with a fiduciary obligation attached, or whether it is informational content dressed up in advisory language.

Robo-Advisors and the Fiduciary Question

Robo-advisors are the one category in this comparison that actually manages money on your behalf, which is also why the fiduciary question matters more here than anywhere else in this guide.

How robo-advisors differ from chatbots

Robo-advisors like Betterment and Wealthfront actually manage money: they build and rebalance a diversified portfolio using Modern Portfolio Theory and automate tax-loss harvesting across taxable accounts. Because they are registered with the SEC as investment advisers, they owe a fiduciary duty — a legal standard that general-purpose chatbots simply do not meet, no matter how well they can explain the concept of diversification. FINRA’s guidance on artificial intelligence is a useful primer if you want the regulator’s own framing of where AI tools fit into the existing advisory rules.

Limits and regulation

Be wary of claims — even from registered firms and professionals — that AI can guarantee amazing investment returns.

Investor.gov (SEC/NASAA/FINRA joint alert)

Even a well-run robo-advisor optimizes on a narrow set of inputs — your stated goals and risk tolerance — and does not see your whole financial life any more than a general chatbot does. That gap between marketed capability and actual scope is exactly what the SEC targeted in 2024, when it brought «AI-washing» enforcement actions against advisers accused of overstating what their AI systems actually did. Fees on robo-advisors are typically modest but real, and they vary by provider and account type; verify current fees and minimums on each provider’s own disclosures rather than trusting a number from a blog roundup, since these figures change.

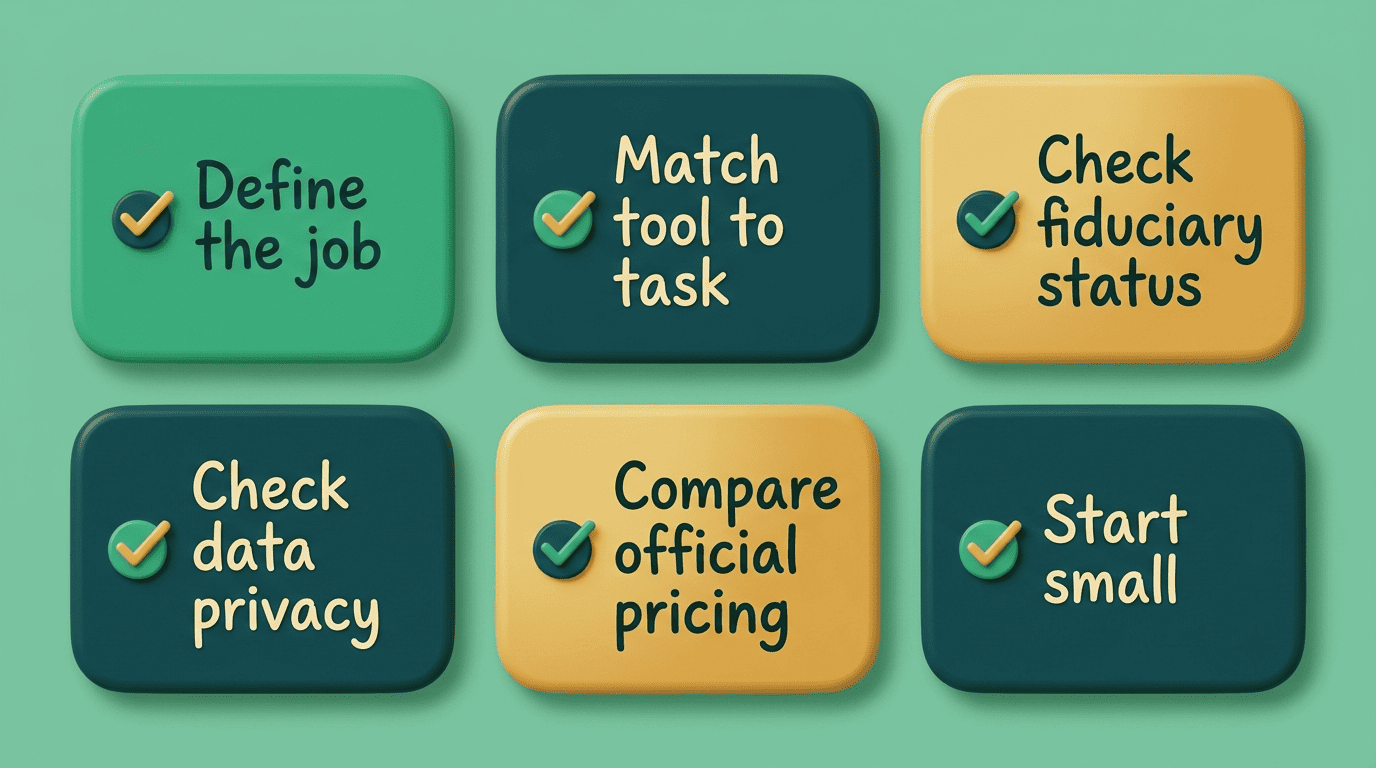

How to Choose: A Practical Selection Framework

The categories above matter less as abstract definitions than as a decision tool — once you know what job you’re hiring a tool for, the right pick tends to be obvious.

- Define the job first. Are you trying to learn a concept, track spending, invest automatically, or plan something complex and tax-sensitive?

- Match the tool to that job, using the framework in the next section.

- Check fiduciary status. Ask directly whether the tool owes you a fiduciary duty, or is purely informational.

- Check where your data goes. Look for a training opt-out option before you connect real accounts or paste in real numbers.

- Compare current pricing on the official site, not a secondhand figure from an article.

- Start small. Test a tool on a low-stakes task before trusting it with anything consequential.

- Loop in a licensed fiduciary for anything genuinely high-stakes or tax-sensitive.

Match the tool to the task

Learning a concept points toward a general LLM assistant. Tracking spending or killing off unwanted subscriptions points toward a dedicated budgeting app. Hands-off, diversified investing points toward a robo-advisor. Complex, high-stakes, tax-sensitive planning points toward a licensed human fiduciary — and no single AI financial advisor tool in this comparison is «best» across all four of those jobs at once, because they were built to do different things.

| If your job is… | Reach for… |

|---|---|

| Learning a financial concept | General LLM assistant (ChatGPT, Gemini, Copilot, Claude) |

| Tracking spending, killing subscriptions | Dedicated budgeting app (Cleo, Rocket Money, YNAB) |

| Hands-off, diversified investing | Robo-advisor (Betterment, Wealthfront) |

| Complex, tax-sensitive planning | Licensed human fiduciary |

Privacy, fiduciary status, and cost

Three checks are worth running before you trust any tool with something real:

- Privacy — never paste your Social Security number, full account numbers, passwords, or an unredacted statement into a general chatbot, and look for a training opt-out where one is offered.

- Fiduciary status — ask directly whether the tool owes you a fiduciary duty (a robo-advisor generally does; a chatbot does not).

- Cost — weigh free chatbots against subscription budgeting apps against a percentage-of-assets robo-advisor fee, comparing each provider’s official current pricing rather than a number quoted in an older roundup.

Can AI Replace a Financial Advisor?

The short answer is no, not for personalized, high-stakes decisions. AI tools are genuinely strong for education, for framing questions, and for routine day-to-day tracking — that much is consistent across every category covered here. For a comprehensive, tax-aware, personalized plan, the consensus across sources like NerdWallet, Fortune, and Wealth Enhancement Group is to use AI tools to prepare and get organized, then work with a licensed fiduciary for the decisions that actually carry consequences. Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.