ChatGPT as an AI Financial Advisor: What It Does Well, What It Can’t, and How to Use It Safely

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

Millions of people now open ChatGPT to ask money questions they used to save for a professional. Used well, an AI financial advisor tool can explain concepts and run budgeting math in plain language, according to guidance from OpenAI’s own help documentation — but it is a study aid, not a fiduciary.

The honest answer: ChatGPT can teach you about money, but it can’t legally or reliably plan your finances for you. This guide covers what it does well, what it can’t (and shouldn’t) do, safe prompts, and when to call a human.

Can ChatGPT Really Act as a Financial Advisor?

ChatGPT is a large language model made by OpenAI, and that single fact shapes everything else in this guide.

What ChatGPT actually is

A large language model predicts likely text based on patterns in its training data — it does not «understand» your finances or verify facts against a live source before answering. A useful way to frame it: a financial co-pilot, not your financial pilot. It’s a learning partner that can sit next to you while you figure things out, not a decision-maker that takes the controls.

The short answer

It can act like a patient teacher and a calculator with words. It cannot act like a licensed advisor who owes you a legal duty. Keep that line clear before you type a single prompt, because the rest of this guide is really about not crossing it.

What ChatGPT Does Well for Personal Finance

Inside its actual strengths, ChatGPT is genuinely useful for the parts of personal finance that are about understanding, not deciding.

Explaining concepts in plain language. Turning jargon (APR vs. APY, Roth vs. traditional, index funds, compound interest) into a plain explanation is a genuine strength. It’s a fast, judgment-free way to learn terms you might otherwise Google five separate times.

Budgeting math and «what-if» scenarios. It can build a simple budget template, run the arithmetic on a debt-payoff schedule, or sketch a savings timeline — as long as you double-check the numbers against your own records or a calculator.

Drafting questions and summarizing documents. It’s useful for drafting a list of questions to bring to a real advisor, or summarizing a long disclosure or prospectus into readable bullets. You still confirm the details against the source document before acting on anything.

| What ChatGPT can help with | What it should not replace |

|---|---|

| Explaining financial terms and concepts | A licensed advisor’s personalized recommendation |

| Drafting a budget template or debt payoff outline | Real-time account monitoring or portfolio management |

| Summarizing a disclosure into plain English | Legal or tax filing decisions |

| Preparing questions for a real advisor meeting | Fiduciary sign-off on a financial plan |

What ChatGPT Can’t — or Shouldn’t — Do

The gap between «helpful explainer» and «advisor» comes down to duty, oversight, and disclosure — three things a chatbot simply doesn’t have.

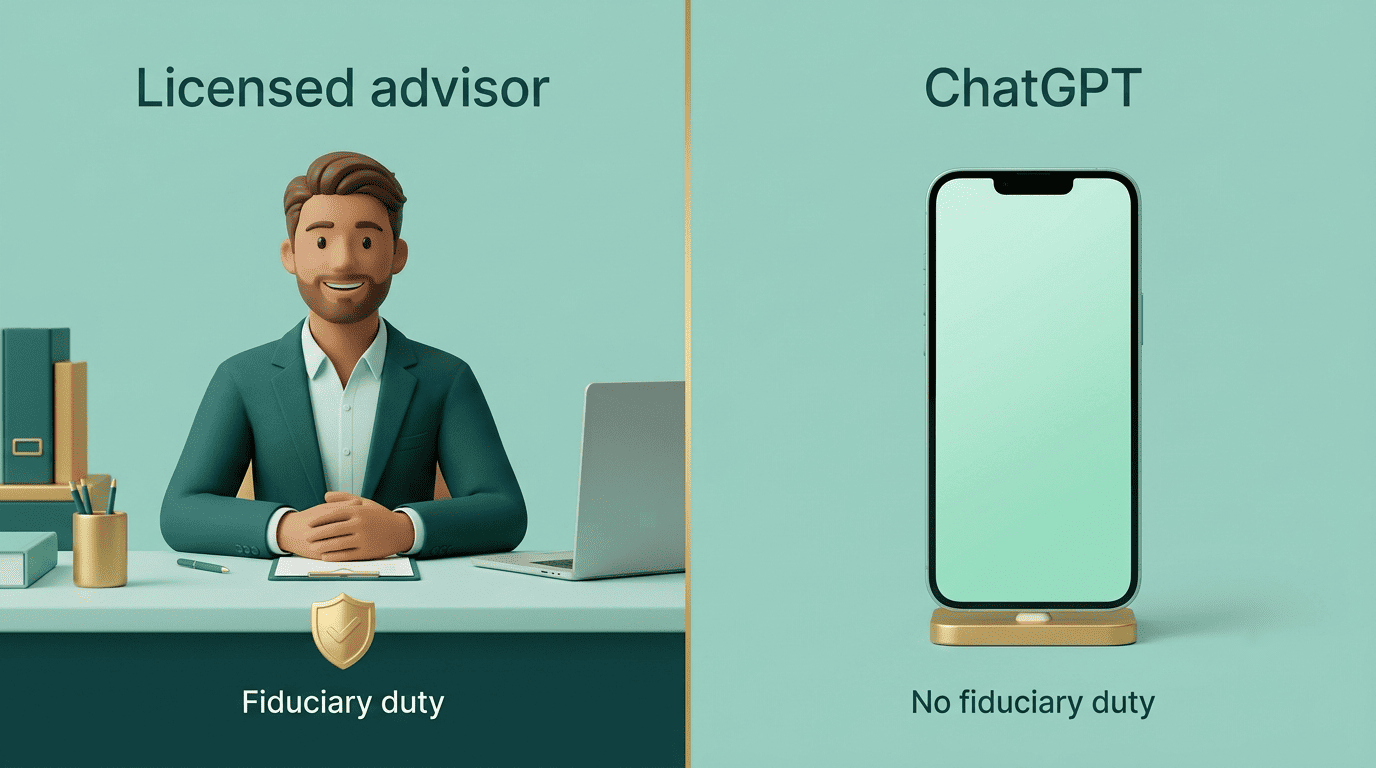

No fiduciary duty and no regulator

A licensed advisor, such as a Certified Financial Planner (CFP) or a registered investment adviser, has a legal duty and sits under oversight from regulators like the SEC and FINRA, with an arbitration process and errors-and-omissions insurance if things go wrong. ChatGPT has no fiduciary duty owed to you, and if its answer harms you, there’s no formal complaint process to turn to.

| Licensed financial advisor (e.g., CFP) | ChatGPT | |

|---|---|---|

| Legal duty to act in your interest | Yes, fiduciary duty | None |

| Regulatory oversight | SEC / FINRA | None |

| Knows your full financial picture | Yes, if disclosed to them | Only what you type in |

| Recourse if advice causes harm | Complaint, arbitration, E&O insurance | None |

| Discloses conflicts of interest | Required by regulation | Not guaranteed |

It can’t assess your whole situation

It doesn’t truly know your risk tolerance, tax bracket, debts, or goals unless you tell it — and even then it can’t weigh them the way a professional who understands the law and sees your full financial picture can.

Undisclosed conflicts and no personalized recommendations

An AI won’t disclose conflicts of interest the way a regulated advisor must. Consider the kind of blind spot this creates: Microsoft has invested billions of dollars in OpenAI, the company behind ChatGPT — and a base model has no built-in obligation to flag a relationship like that if it ever came up in a conversation about a specific company. Treat any specific stock or product «pick» from a chatbot as a red flag, not advice.

Accuracy and Hallucinations: The Biggest Risk

If fiduciary duty is the legal gap, hallucination is the practical one — and it’s the risk most likely to bite you without warning.

«Confidently wrong» is the failure mode

Hallucination means the model states false information as fact, and it does so fluently, with no hedge in its tone to warn you. This is a well-documented weakness of large language models in general, and finance is no exception: an incorrect number about a tax rule or a loan calculation can read exactly as confident as a correct one.

Numbers and current data are weak spots

Research led by Andrew Lo at MIT Sloan examined whether a general-purpose model like ChatGPT can meet the bar for reliable financial guidance on its own — and found that it falls short without extra help. A base model also has no live data connection by default: it doesn’t know today’s interest rates, market prices, or your account balance unless it’s specifically connected to a source that provides them.

Doesn’t quite pass, but it’s close. It’s actually remarkably close.Andrew Lo, MIT Sloan School of Management

Live Account Access and Privacy

Before you connect anything financial to a chatbot, it helps to know exactly what «connect» means in practice.

Does ChatGPT see your bank account?

Not by default. A standalone chat has no access to your accounts. Some newer connected features can link financial data through account-aggregation providers such as Plaid, which changes the privacy calculus considerably — read carefully what you’re authorizing before you approve any connection.

What never to paste into a chatbot

Treat any AI tool that touches your financial data the way you’d treat an unfamiliar app: assume prompts may be stored or reviewed, and keep inputs generic and anonymized wherever possible. Never share the following in a chat:

- Social Security numbers

- Full bank or brokerage account numbers

- Login credentials or passwords

- Complete personal financial statements tied to your identity

This approach lines up with general guidance from the Consumer Financial Protection Bureau on protecting sensitive financial data online.

Good Prompt Examples (and Bad Ones)

The line between a useful prompt and a risky one usually comes down to whether you’re asking it to teach you something or to decide something for you.

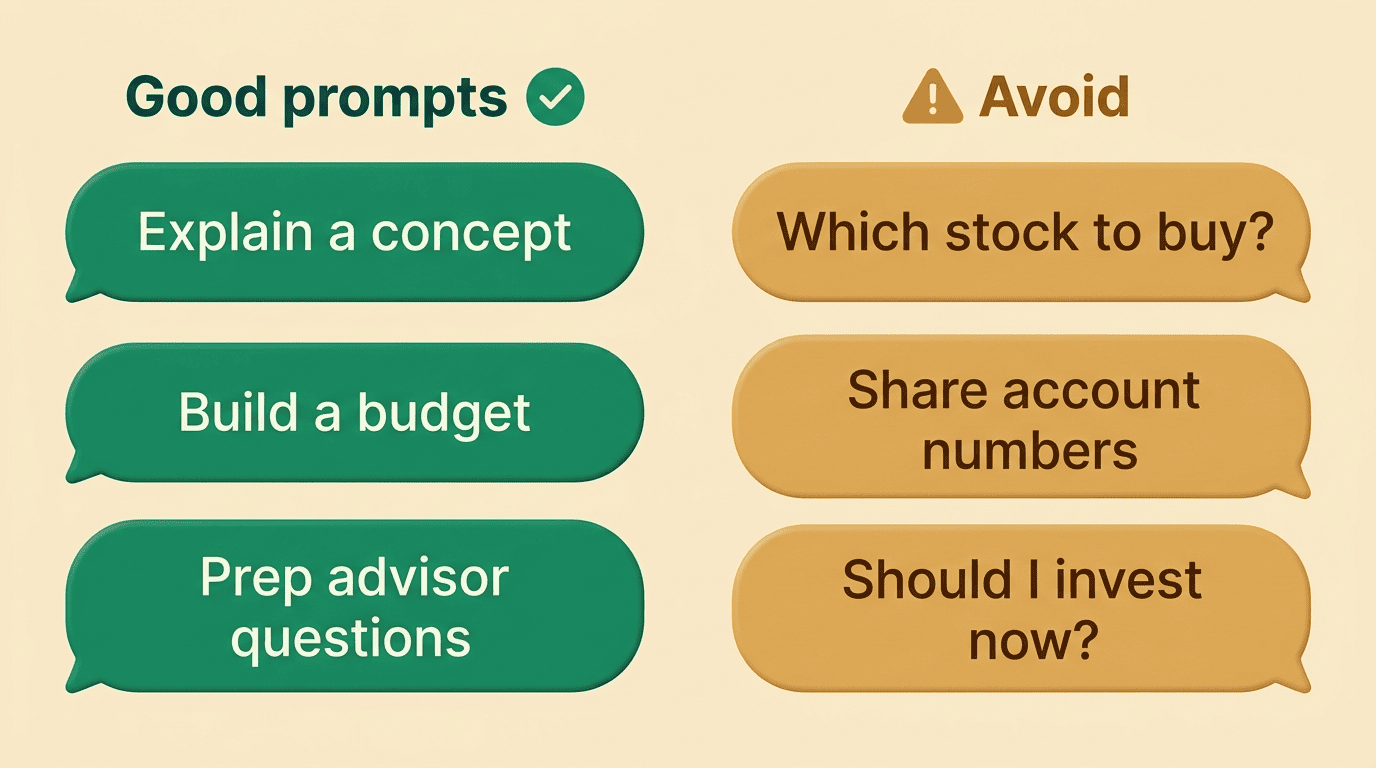

Prompts that play to its strengths

- «Explain the difference between a Roth and traditional IRA in simple terms.»

- «Help me build a monthly budget template from these categories.»

- «Summarize this 401(k) disclosure into plain-English bullet points.»

- «What questions should I ask a financial advisor about retirement?»

- «Walk me through how compound interest works with an example.»

Prompts to avoid (red flags)

- «Which specific stock should I buy right now?»

- «Should I put my savings into X?» — a base model has no live market data and no duty to act in your interest.

- Pasting real account numbers, balances tied to your identity, or Social Security numbers into any chat.

How to Use ChatGPT Safely as a Money Tool

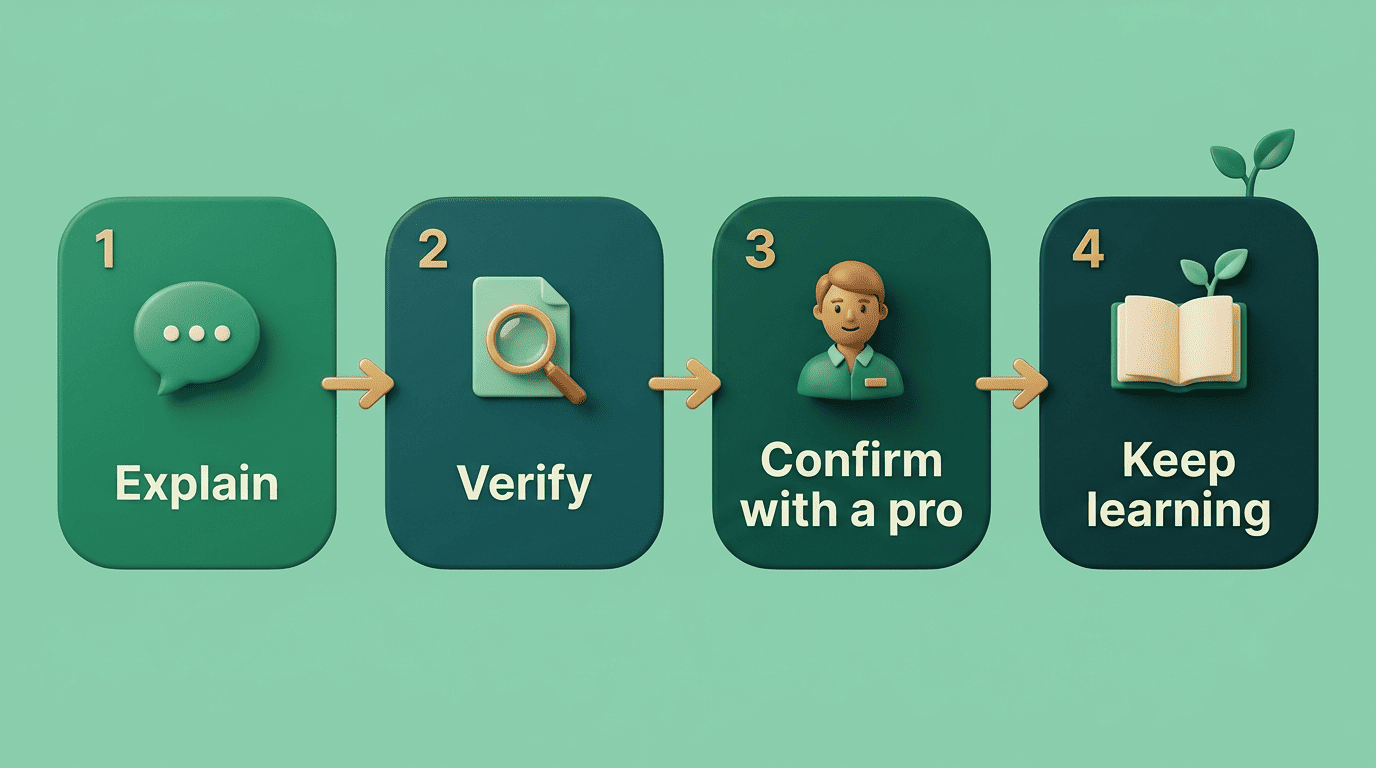

Turning the strengths and limits above into a habit is simpler than it sounds — it comes down to four repeatable steps.

A simple four-step habit

- Ask it to explain, not decide.

- Verify any number or rule against a primary source before you rely on it.

- Confirm real decisions with a licensed professional.

- Use it to keep learning between those confirmations.

This is where an AI-powered financial advisor tool adds real value — as a tutor that gets you ready for a human conversation, not a replacement for one.

When you must talk to a human

A short list of situations that warrant a licensed advisor, not a chatbot:

- Filing or planning around taxes

- Making a large investment move

- Planning a retirement drawdown strategy

- Choosing or changing insurance coverage

- Estate planning

- Working through serious debt decisions

You can use Investor.gov to check a professional’s background before you hire them. An AI financial advisor tool can help prepare your questions, but a fiduciary should sign off on the actual plan.