How to Use an AI Financial Advisor to Pay Off Debt: Snowball vs Avalanche, Step by Step

Paying off debt is less about willpower and more about a clear, prioritized plan. An AI financial advisor can turn a messy pile of balances and interest rates into a step-by-step payoff order in seconds, the same way a debt calculator from Fidelity walks through the math, just conversational.

This guide shows how to feed your debts to an AI money coach, choose between the snowball and avalanche methods, and — importantly — when to step away from any app and call a nonprofit credit counselor instead.

Educational information only — not financial advice, and not a substitute for a licensed financial advisor. Consult a professional before making financial decisions.

What an AI Financial Advisor Can (and Can’t) Do for Debt

An AI-powered financial advisor is a conversational tool that organizes your numbers, explains options in plain English, and models different payoff scenarios instantly. It helps you build a listed, prioritized debt payoff plan out of a pile of balances, APRs, and minimum payments — work that used to mean a spreadsheet and a calculator.

Sort and re-sort your debts on request. Ask it to reorder six debts by APR or by balance and it answers immediately, applying the same arithmetic a spreadsheet does, just faster to talk through.

Model «what if» scenarios in seconds. Add $50 or $100 a month to the plan and it recalculates the payoff date and total interest without you touching a formula.

Draft a plan you still have to review. The output is a starting point, not a verdict — you check the numbers against your actual statements before acting on them.

What it should not do: give you personalized regulated financial advice, act as a fiduciary, negotiate directly with your creditors, or account for your full legal and tax situation. A general AI financial advisor tool can surface math, not judgment about your life — treat everything it produces as a draft to review, not a final answer.

The strengths: math, structure, and instant «what-ifs»

It never tires of recalculating. Ask it to re-order six debts or model an extra $50 a month and it answers immediately — the same arithmetic a spreadsheet does, just faster to talk to.

The limits: no fiduciary duty, no full picture

It doesn’t know your job security, health, or state laws, and general chatbots are not licensed advisors. Treat output as a draft to review, and keep the disclaimer above in mind before you act on any suggested plan.

Step 1: List Every Debt (Balance, APR, Minimum Payment)

The single most important input is a complete, honest list. A workable debt payoff plan requires listing every debt with its balance, APR, and minimum payment — skip one card and the whole ordering can come out wrong.

| Field | What to include |

|---|---|

| Lender/name | Credit card issuer, bank, or loan servicer |

| Current balance | Exact amount owed today, not the credit limit |

| APR | The interest rate that accrues on the balance |

| Minimum monthly payment | The amount due even if you pay nothing extra |

| Debt type | Credit card, personal loan, auto loan, private student loan |

Why APR matters more than balance

APR is what the debt costs you every month. A $1,300 card at 22% APR is more expensive per dollar than a $10,000 loan at 6%. Getting these numbers right is what lets an AI, or you working from a notepad, prioritize correctly.

A note before you paste anything sensitive

Share only what you’re comfortable with; avoid full account numbers and Social Security numbers. Pairing a debt plan with a monthly budget makes the numbers easier to trust — see our guide on budgeting with an AI financial advisor alongside a payoff plan.

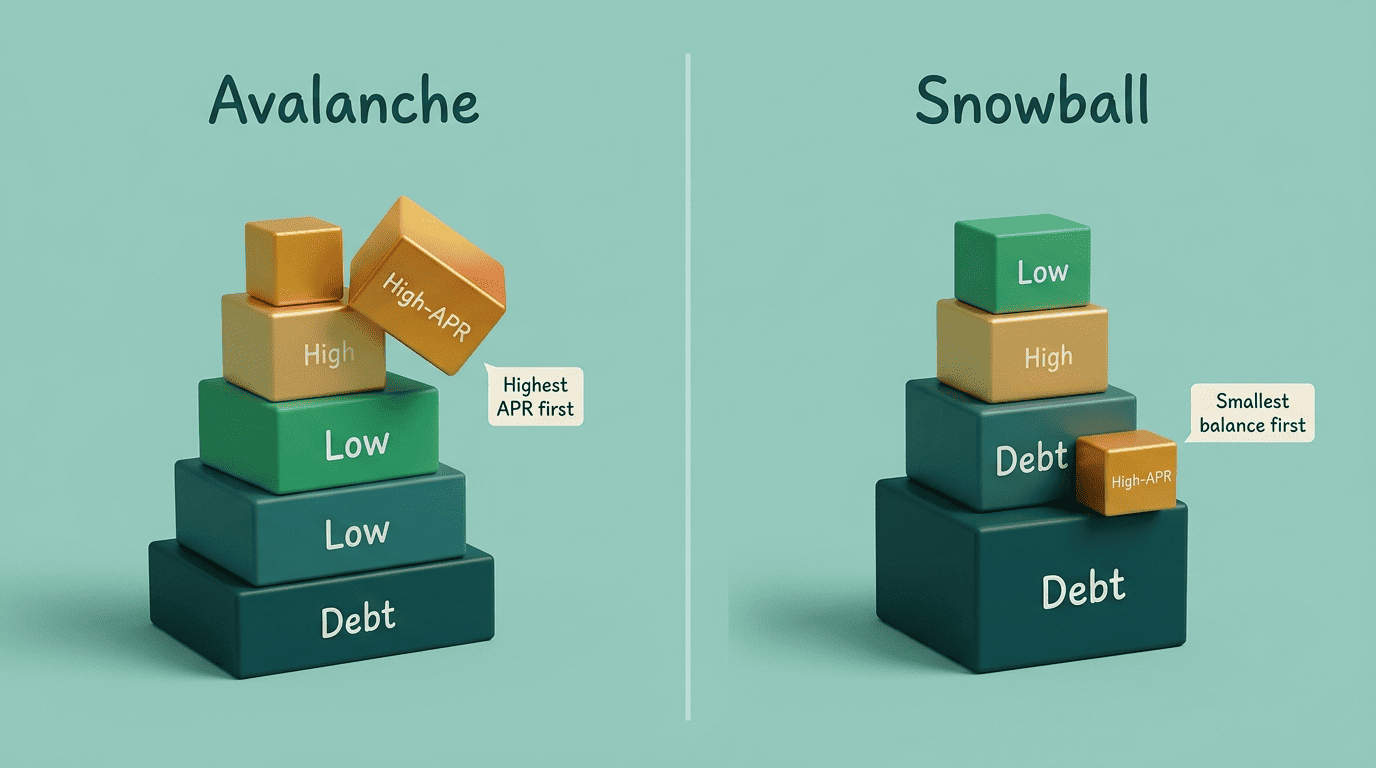

Debt Snowball vs Debt Avalanche: The Two Core Strategies

Both methods pay minimums on everything and throw every spare dollar at one target debt. They differ only in which debt is the target — and both require paying more than the minimum on that one debt each month.

| Debt avalanche | Debt snowball | |

|---|---|---|

| Target debt | Highest APR first | Smallest balance first |

| Optimizes for | Total interest saved | Early motivation, quick wins |

| Typical trade-off | Can feel slow if the highest-APR debt is also large | Usually costs a little more interest overall |

The avalanche method: highest APR first (saves the most interest)

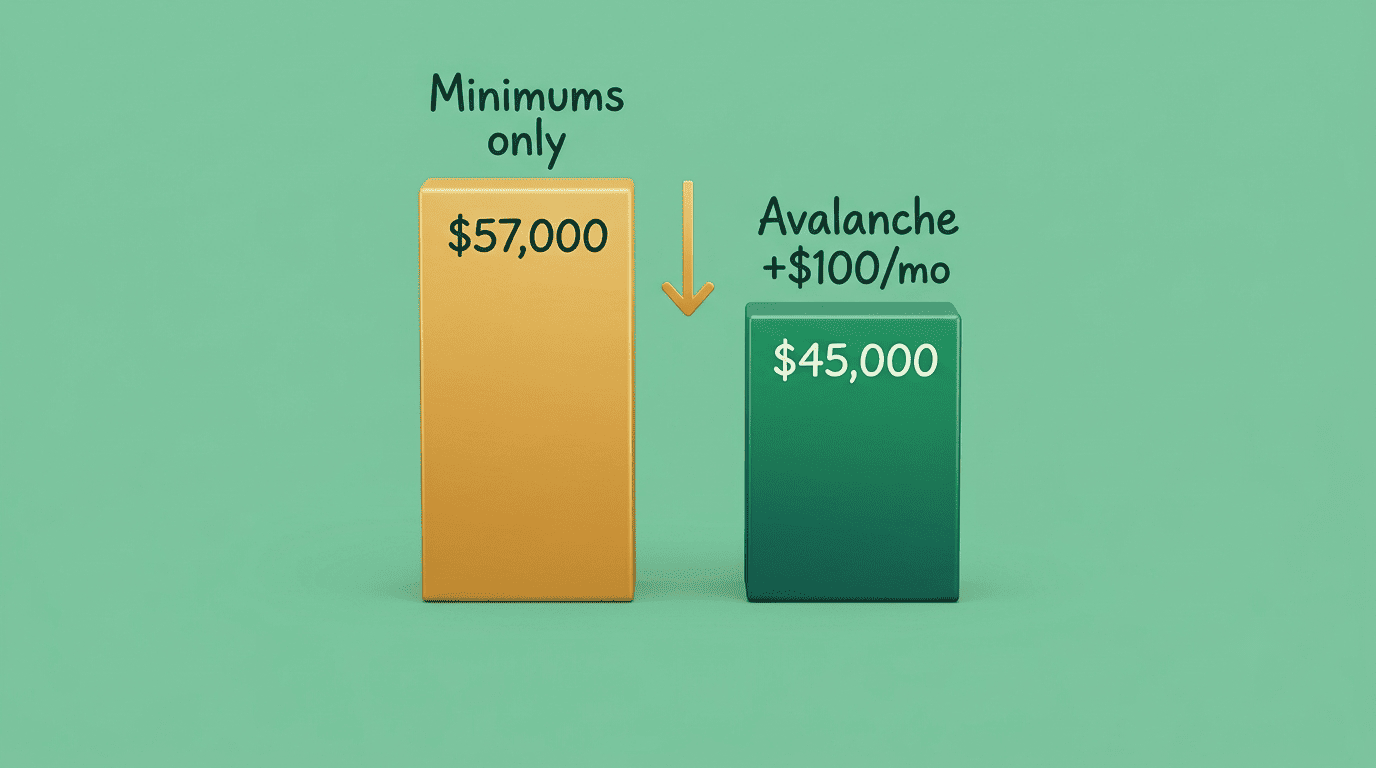

The debt avalanche method prioritizes the debt with the highest interest rate first. Order every debt from highest APR to lowest and attack the top one while paying minimums on the rest — it’s the mathematically cheapest route. Fidelity’s illustration shows that with an extra $100 a month, an avalanche payoff saved roughly $12,000 in interest and finished about three years sooner than paying minimums only.

The snowball method: smallest balance first (best for motivation)

The debt snowball method prioritizes the smallest balance first, popularized by financial personality Dave Ramsey. Order debts from smallest balance to largest and knock out the small ones for quick wins. Discover notes it taps a «small wins» effect that matters given how many people report money-related stress. It usually costs a little more interest than the avalanche method.

Which actually wins? It depends on your numbers

Often the gap is small. In CNBC Select’s worked example — four debts totaling several thousand dollars, paid down at $650 a month — the avalanche method saved about $153 in interest and finished in 40 months versus 41 for the snowball method. Experian shows that in some debt mixes, the snowball method can even edge out the avalanche method on total interest. The best method is the one you’ll actually stick with.

The «snowflake» add-on

The snowflake method applies small windfalls — a $20 rebate, a side-gig payment — to your target debt as they arrive. It works alongside either the snowball or the avalanche method and simply speeds up whichever plan you’ve chosen.

Step 2: Let the AI Prioritize and Model Your Timeline

Once your list is in, ask the AI financial advisor tool to sort it both ways and show payoff dates. This is where the tool shines: comparing «avalanche vs snowball for my debts» with real timelines and total-interest figures, then testing an extra $50 or $100 a month to see how much time and interest it saves. It’s also worth asking it to flag when a different route — a debt consolidation loan or a 0% APR balance transfer card — might beat either method, since consolidating high-APR balances into one lower-rate payment can sometimes save more than reordering them.

Prerequisites the AI should remind you of

- Confirm you have a small emergency fund first — Fidelity suggests 3 to 6 months of essential expenses — so a surprise expense doesn’t push you back onto the cards.

- Never miss a minimum payment on any debt; a missed payment can hurt your credit score even while you’re aggressively paying down another balance.

- Recheck your list every month, since balances, APRs, and even minimum payments can change.

- Ask the AI to re-run both methods whenever your income or extra-payment amount changes.

Sample Prompts for an AI Debt-Payoff Planner

Concrete prompts get concrete answers. Try feeding an AI financial advisor tool something like these:

- «Here are my debts [list balance, APR, minimum]. Sort them for the avalanche method and estimate my payoff date if I add $100/month.»

- «Compare snowball vs avalanche for these debts and show total interest for each.»

- «I have $300 extra this month — which debt should it go to under each method?»

- «Explain, in plain English, why my highest-APR card costs more than my bigger loan.»

When to Skip the App: Nonprofit Credit Counseling

If you’re only making minimum payments, falling behind, or feeling in crisis, an AI plan isn’t enough — talk to a person. Nonprofit credit counseling agencies, findable through the NFCC, review your whole budget for free and can set up a debt management plan. A counselor negotiates lower rates and waived fees with your creditors, you make one monthly deposit instead of several, and unsecured debts are typically cleared within three to five years.

Debt settlement may well leave you deeper in debt than you were when you started.

Consumer Financial Protection Bureau

Signs it’s time to call a counselor

Any of the following is a signal to reach out, not just keep tweaking the AI’s plan:

- Using one card to pay off another card’s balance

- Only ever managing the minimum payment, never more

- Getting regular collection calls or letters

- Debt payments crowding out rent, food, or other essentials

This is judgment an app can’t provide.

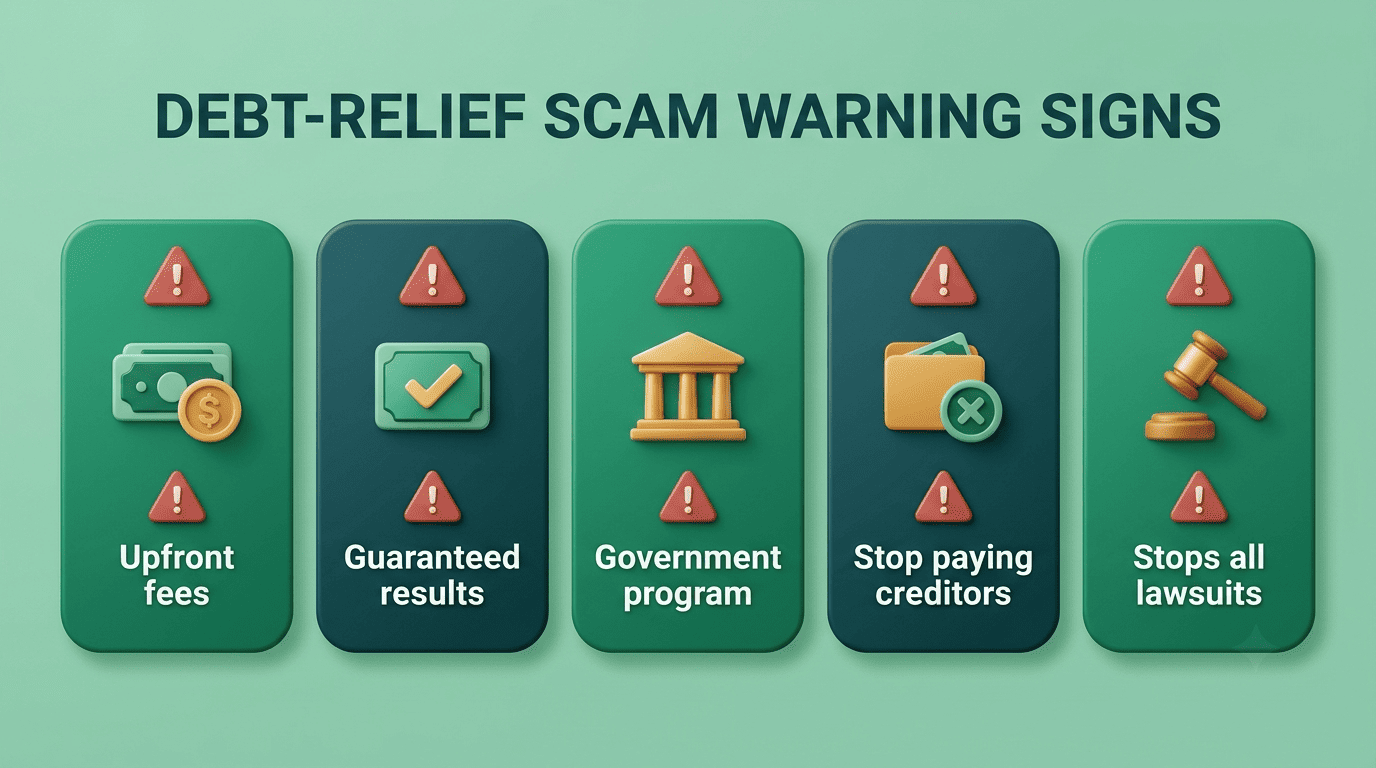

Beware Debt-Relief and Debt-Settlement Scams

For-profit debt settlement is not the same as nonprofit credit counseling and can be risky. Per the FTC and CFPB, treat these as red flags — walk away if a company:

- charges fees before settling any debt (this is illegal),

- guarantees to make your debt «go away» or settle for «pennies on the dollar,»

- pushes a «new government program,»

- tells you to stop communicating with your creditors,

- promises to stop all collection calls and lawsuits.

Also note: settled or forgiven debt can count as taxable income. When in doubt, verify a company with the CFPB or FTC before signing anything.